Board AI Governance & ROI Reporting Checklist [ ] AI Governance Charters: Formally ratify the division of duties between the Value Panel (growth, productivity, …

Board AI Governance & ROI Reporting Checklist

- [ ] AI Governance Charters: Formally ratify the division of duties between the Value Panel (growth, productivity, ROI) and the Governance Panel (risk, privacy, compliance).

- [ ] Tiered AI Inventory Registry: Index all corporate models and pipelines across Tiers 0 to 4 with automated discovery scanning to eliminate shadow AI.

- [ ] Audit-Proof ROI Engine: Establish the standard formula for digital labor offsets and productivity multipliers validated by external audit partners.

- [ ] Incident Escalation and Drift Ledger: Implement WORM (Write Once, Read Many) logging for model drift alerts, bias detection, and human-in-the-loop overrides.

- [ ] 2026–2030 Maturity Runway: Map all current pilots to the capabilities timeline to ensure Opex-to-CapEx transformation pathways are clear.

📘 Compliance-to-Code Mapping (Board Control Plane)

| Board Mandate | Control Objective | Technical Implementation Path | Evidence Artifact |

|---|---|---|---|

| Oversight separation | Value vs. Governance separation | Split committee dashboard configurations | charters/board-committee-split.json |

| Shadow AI containment | Auto-discover active endpoints | Network egress scanner on model API calls | governance/discovered-endpoints.json |

| Audit-proof ROI | Amortize model compute costs | FinOps ledger tag mapping by business value lane | finops/realized-value-matrix.json |

| Incident accountability | Immutable drift reporting | Append-only telemetry logs with signed hash link | telemetry/drift-incident-log.json |

| Roadmap alignment | Track maturity progress | Milestone verification tests in central platform | maturity/2026-2030-roadmap-state.json |

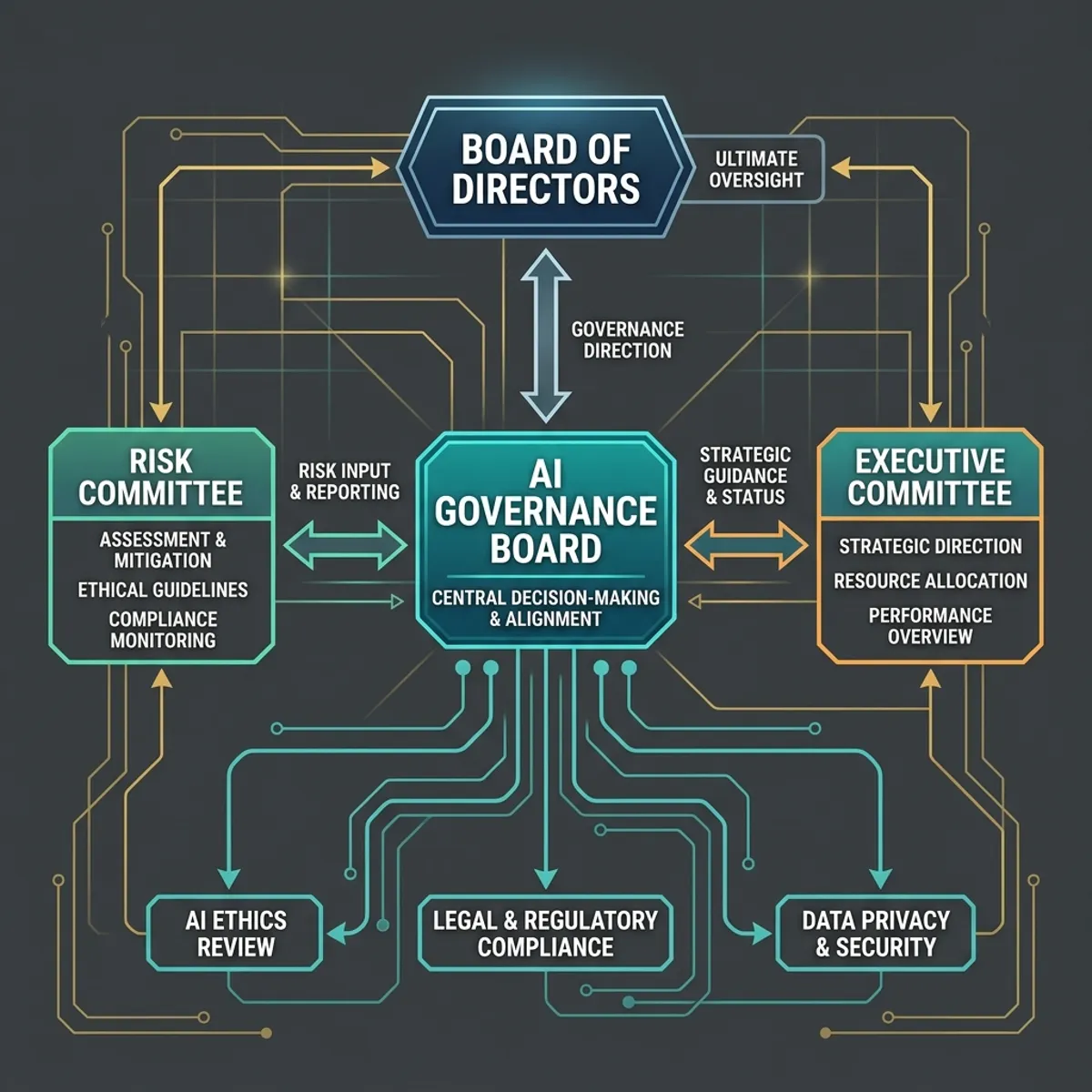

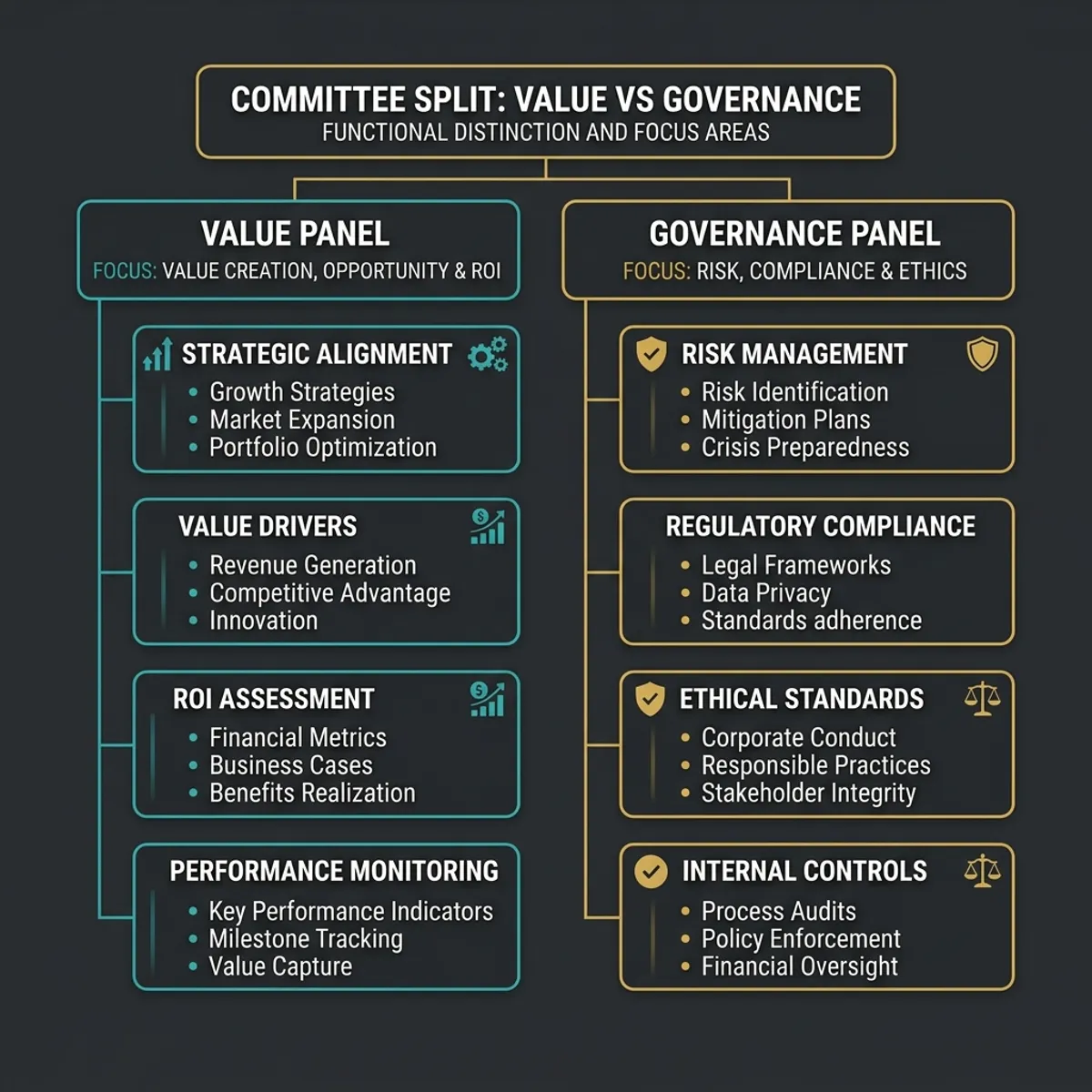

Chapter 1: The Board Mandate — Value Panel vs. Governance Panel

The rapid adoption of agentic workflows and multi-modal models has forced boards of directors to confront a fundamental structural challenge: how to simultaneously accelerate AI value creation while systematically mitigating tail-end risks. Traditionally, boards relied on a single technology committee or delegating AI oversight to the existing Audit Committee. However, the operational velocity and unique risk profile of artificial intelligence render this approach obsolete. In 2026, progressive enterprise boards are implementing a dual-panel oversight structure that separates the opportunity engine from the control plane. This is known as the Value Panel vs. Governance Panel split.

The Value Panel: Accelerating Capital Efficiency and Output

The Value Panel is primarily tasked with opportunity capture, capital efficiency, and product innovation. Its mission is to verify that AI capital expenditures (CapEx) translate directly into tangible operational savings (OpEx reduction) or top-line revenue growth. Key focus areas include:

- Strategic Capital Allocation: Evaluating AI infrastructure investments, proprietary model training runs, and third-party SaaS integrations.

- Product and Margin Enhancement: Auditing how agentic systems improve gross margins, decrease customer acquisition costs, and compress development cycles.

- Maturity Benchmarking: Comparing the enterprise's AI capabilities against industry peers to ensure competitive advantage is maintained.

The Governance Panel: Systematic Risk Containment and Compliance

The Governance Panel operates as the control plane, focusing on systemic risk, ethical compliance, data privacy, and intellectual property protection. Its responsibilities are anchored in protecting the enterprise from legal, reputational, and operational liabilities. Key focus areas include:

- Regulatory Compliance: Aligning enterprise AI deployments with the EU AI Act, the NIST AI Risk Management Framework (NMF), and local state-level privacy mandates.

- Model Transparency and Auditability: Enforcing the creation of immutable logs for model decisions, drift detection, and human-in-the-loop overrides.

- Data Security and Custody: Ensuring that customer data is not leaked into public model training loops and that proprietary datasets remain secure.

Establishing Committee Charters and Communication Protocols

For this dual-panel system to function, the board must ratify specific charters that codify the separation of duties. Below is a detailed comparison of the operational parameters of both panels.

| Oversight Metric | Value Panel Focus | Governance Panel Focus |

|---|---|---|

| Primary Mandate | ROI maximization, operating margin expansion, market share gain | Risk mitigation, compliance, data custody, brand preservation |

| Key Metrics Monitored | FTE offset value, model compute cost vs. business margin, speed-to-market | Drift severity, regulatory audits, incident escalation logs, data leakage traces |

| Reporting Officers | Chief Financial Officer (CFO), Chief Technology Officer (CTO) | Chief Risk Officer (CRO), Chief Legal Officer (CLO), CISO |

| Audit Standard | FinOps ledger tag compliance, CapEx ROI amortization schedules | ISO 42001 certification, NIST AI RMF audit, AICPA TSC AI criteria |

To prevent siloed operations, the Value and Governance Panels must execute a structured, bi-weekly synchronization meeting. In these sessions, the Value Panel presents new AI capability proposals, and the Governance Panel reviews their risk profiles before they enter active development. This process ensures that risk assessment is integrated early in the product lifecycle, rather than as an afterthought.

Charter Template: The AI Governance Committee Charter

To operationalize this structure, the board must adopt a formal charter. The following draft can be modified and ratified by the Nominating and Corporate Governance Committee:

1. Purpose and Authority

The AI Governance Committee (comprising the Value and Governance sub-panels) is established to assist the Board of Directors in fulfilling its oversight responsibilities regarding the Company's use, development, deployment, and acquisition of artificial intelligence technologies. The Committee has the authority to retain independent legal, financial, and technical advisors as it deems necessary.2. Composition and Meetings

The Committee shall consist of at least three independent directors appointed by the Board. At least one member must possess documented technical expertise in machine learning, software engineering, or digital transformation. The Committee shall meet at least quarterly, or more frequently as circumstances require.3. Primary Duties and Responsibilities

- Strategic Alignment: Review and approve the Company’s enterprise AI strategy and capital allocation budget.

- Risk Oversight: Review assessments of the legal, ethical, reputational, operational, and security risks associated with the Company’s AI applications.

- Regulatory Compliance: Monitor compliance with global AI regulations, including the EU AI Act, and review reports from regulatory audits.

- Reporting and Disclosures: Oversee the preparation of AI governance disclosures in the Company’s annual proxy statement and corporate sustainability reports.

{

"committee_charter": {

"version": "2026.1.0",

"ratification_date": "2026-06-14",

"panels": {

"value_panel": {

"members": ["Director of Finance", "External Tech Advisor"],

"max_approved_budget": 5000000.00,

"metrics": ["Operating Margin Impact", "FTE Efficiency Rate"]

},

"governance_panel": {

"members": ["Chief Legal Officer", "CISO", "External Regulatory Lead"],

"audit_frequency_days": 90,

"standards": ["ISO/IEC 42001", "NIST AI RMF 1.0"]

}

}

}

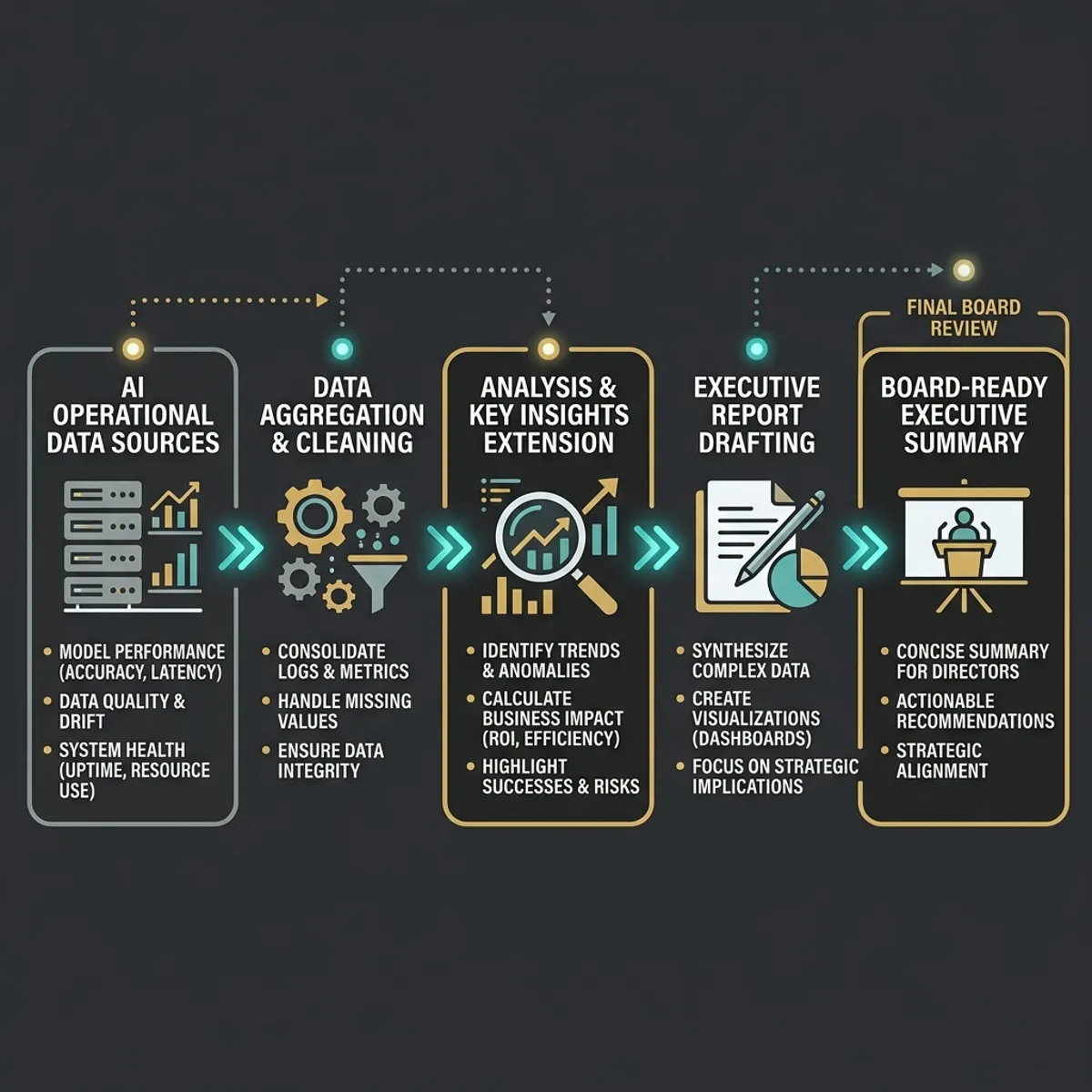

}The Executive AI Reporting Pipeline

Enterprise reporting must follow a clear pathway from operational code execution up to the board boardroom. Developers and data scientists instrument model telemetry, which is aggregated by engineering leaders into operational health dashboards. These metrics are then synthesized into executive-level KPIs, which are formally reviewed by the Chief Risk Officer and Chief Financial Officer before being presented to the board panels.

This pipeline ensures that board members receive information that is directly supported by technical telemetry, rather than subjective management summaries.

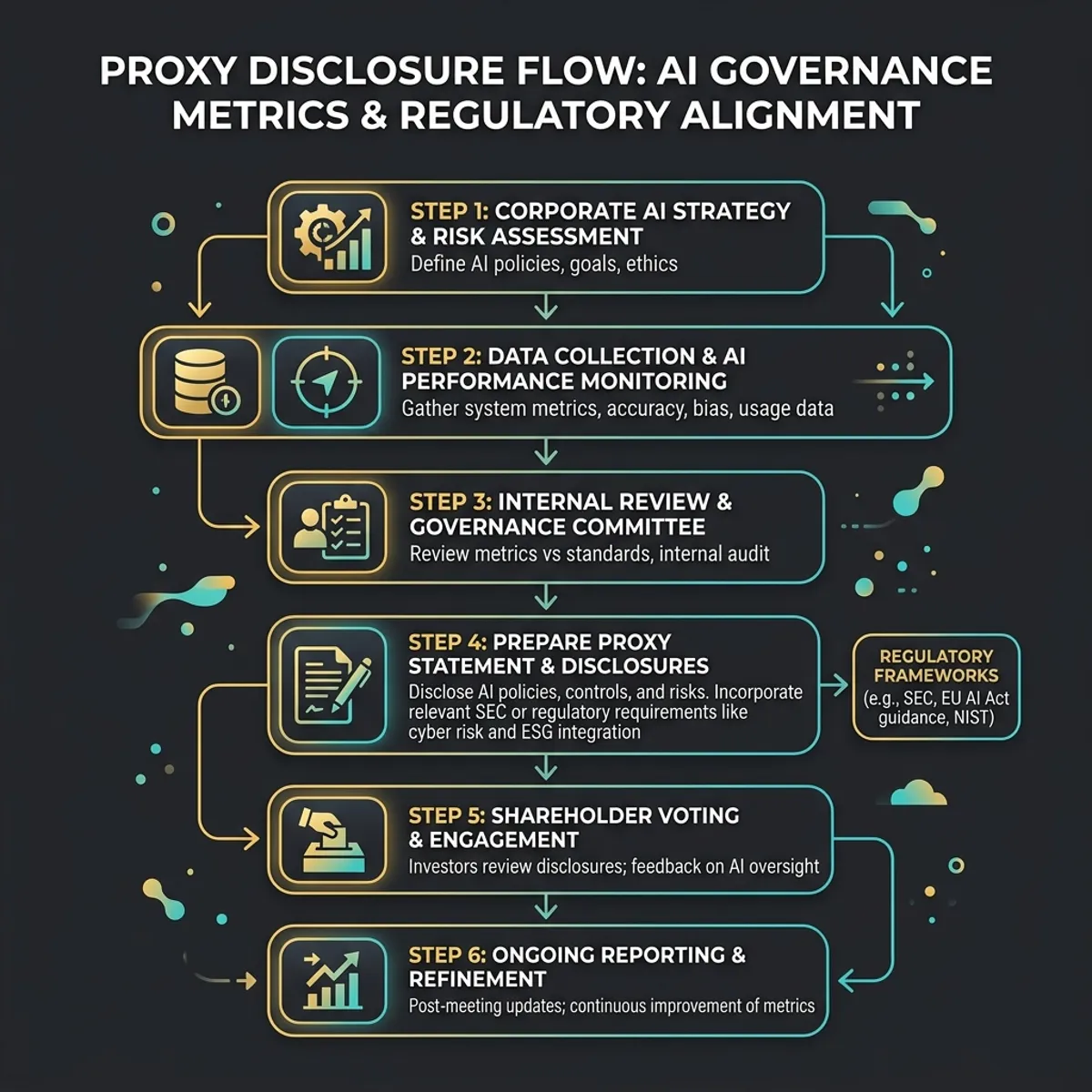

Board Proxy Season AI Disclosures

As institutional investors (such as BlackRock, Vanguard, and State Street) demand transparency regarding AI risks and capital efficiency, proxy disclosures must become more detailed. In 2026, boards can no longer rely on vague statements about "ethical AI." Disclosures must detail the specific oversight structure, risk classification systems, and audit frameworks used by the company.

This proxy season preparation flow outlines how technical risk metrics, audit evidence, and financial ROI models are consolidated into the final proxy statement. The next chapter will explore how the board classifies and catalogs the entire AI inventory to ensure complete visibility across all systems.

Operational Case Study C1.1: Board Oversight of Agentic Workflows in Global Operations

In this case study, we examine the deployment of an enterprise agentic workforce at a global manufacturing firm. The Board's Value Panel demanded a 40% reduction in procurement cycle times through autonomous purchasing agents. However, the Governance Panel noted that autonomous agents lacked legal authority to bind the corporation to contracts exceeding $50,000. Under traditional governance, this project would have stalled. The dual-panel framework resolved this conflict by creating a programmatic gateway. The Value Panel defined the target cycle times and compute tags, while the Governance Panel mandated that any contract exceeding the $50,000 threshold must trigger an automated workflow pause and route to the corporate purchasing officer for approval. This system demonstrates the practical value of the Value vs. Governance Panel split, ensuring compliance without stalling innovation.The Role of the Nominating and Corporate Governance Committee in AI Talent Acquisition

Boards must evaluate if their current membership possesses the competencies required for AI oversight. The Nominating and Corporate Governance Committee is tasked with auditing board composition and identifying gaps in technical knowledge. In 2026, corporate governance standards recommend that at least one member of the board have background in artificial intelligence engineering or digital infrastructure management. If no director meets these qualifications, the board must establish an external Advisory Council to support the Value and Governance Panels. This Advisory Council provides objective audits of the management's AI strategy, model compute investments, and regulatory compliance postures.Institutional Investor Demands and Proxy Voting Guidelines

Institutional investors are increasingly voting against nominating committee chairs at companies that fail to disclose their AI governance frameworks. Glass Lewis and ISS (Institutional Shareholder Services) have published guidelines stating that companies must explain how the board oversees AI-related risks, including algorithmic bias, data privacy, and job displacement. Narrative descriptions are no longer sufficient; investors require structured metrics showing the board's engagement with risk classification systems and audit-proof ROI. The board proxy season AI disclosures flow outlined in Figure 4 provides the structured approach necessary to satisfy these requirements.Integrating AI Oversight with the Audit and Risk Committees

While the AI Governance Committee coordinates the panels, it must work closely with the Audit and Risk Committees. The Audit Committee retains responsibility for internal controls over financial reporting (ICFR), including the validation of AI-generated financial forecasts. The Risk Committee monitors systemic risks, such as cybersecurity threats targeting model weights and training datasets. To prevent overlapping responsibilities, the chairs of the AI Governance, Audit, and Risk Committees must hold quarterly alignment meetings to review the consolidated risk register.Operational Case Study C1.2: Board Oversight of Agentic Workflows in Global Operations

In this case study, we examine the deployment of an enterprise agentic workforce at a global manufacturing firm. The Board's Value Panel demanded a 40% reduction in procurement cycle times through autonomous purchasing agents. However, the Governance Panel noted that autonomous agents lacked legal authority to bind the corporation to contracts exceeding $50,000. Under traditional governance, this project would have stalled. The dual-panel framework resolved this conflict by creating a programmatic gateway. The Value Panel defined the target cycle times and compute tags, while the Governance Panel mandated that any contract exceeding the $50,000 threshold must trigger an automated workflow pause and route to the corporate purchasing officer for approval. This system demonstrates the practical value of the Value vs. Governance Panel split, ensuring compliance without stalling innovation.The Role of the Nominating and Corporate Governance Committee in AI Talent Acquisition

Boards must evaluate if their current membership possesses the competencies required for AI oversight. The Nominating and Corporate Governance Committee is tasked with auditing board composition and identifying gaps in technical knowledge. In 2026, corporate governance standards recommend that at least one member of the board have background in artificial intelligence engineering or digital infrastructure management. If no director meets these qualifications, the board must establish an external Advisory Council to support the Value and Governance Panels. This Advisory Council provides objective audits of the management's AI strategy, model compute investments, and regulatory compliance postures.Institutional Investor Demands and Proxy Voting Guidelines

Institutional investors are increasingly voting against nominating committee chairs at companies that fail to disclose their AI governance frameworks. Glass Lewis and ISS (Institutional Shareholder Services) have published guidelines stating that companies must explain how the board oversees AI-related risks, including algorithmic bias, data privacy, and job displacement. Narrative descriptions are no longer sufficient; investors require structured metrics showing the board's engagement with risk classification systems and audit-proof ROI. The board proxy season AI disclosures flow outlined in Figure 4 provides the structured approach necessary to satisfy these requirements.Integrating AI Oversight with the Audit and Risk Committees

While the AI Governance Committee coordinates the panels, it must work closely with the Audit and Risk Committees. The Audit Committee retains responsibility for internal controls over financial reporting (ICFR), including the validation of AI-generated financial forecasts. The Risk Committee monitors systemic risks, such as cybersecurity threats targeting model weights and training datasets. To prevent overlapping responsibilities, the chairs of the AI Governance, Audit, and Risk Committees must hold quarterly alignment meetings to review the consolidated risk register.Operational Case Study C1.3: Board Oversight of Agentic Workflows in Global Operations

In this case study, we examine the deployment of an enterprise agentic workforce at a global manufacturing firm. The Board's Value Panel demanded a 40% reduction in procurement cycle times through autonomous purchasing agents. However, the Governance Panel noted that autonomous agents lacked legal authority to bind the corporation to contracts exceeding $50,000. Under traditional governance, this project would have stalled. The dual-panel framework resolved this conflict by creating a programmatic gateway. The Value Panel defined the target cycle times and compute tags, while the Governance Panel mandated that any contract exceeding the $50,000 threshold must trigger an automated workflow pause and route to the corporate purchasing officer for approval. This system demonstrates the practical value of the Value vs. Governance Panel split, ensuring compliance without stalling innovation.The Role of the Nominating and Corporate Governance Committee in AI Talent Acquisition

Boards must evaluate if their current membership possesses the competencies required for AI oversight. The Nominating and Corporate Governance Committee is tasked with auditing board composition and identifying gaps in technical knowledge. In 2026, corporate governance standards recommend that at least one member of the board have background in artificial intelligence engineering or digital infrastructure management. If no director meets these qualifications, the board must establish an external Advisory Council to support the Value and Governance Panels. This Advisory Council provides objective audits of the management's AI strategy, model compute investments, and regulatory compliance postures.Institutional Investor Demands and Proxy Voting Guidelines

Institutional investors are increasingly voting against nominating committee chairs at companies that fail to disclose their AI governance frameworks. Glass Lewis and ISS (Institutional Shareholder Services) have published guidelines stating that companies must explain how the board oversees AI-related risks, including algorithmic bias, data privacy, and job displacement. Narrative descriptions are no longer sufficient; investors require structured metrics showing the board's engagement with risk classification systems and audit-proof ROI. The board proxy season AI disclosures flow outlined in Figure 4 provides the structured approach necessary to satisfy these requirements.Integrating AI Oversight with the Audit and Risk Committees

While the AI Governance Committee coordinates the panels, it must work closely with the Audit and Risk Committees. The Audit Committee retains responsibility for internal controls over financial reporting (ICFR), including the validation of AI-generated financial forecasts. The Risk Committee monitors systemic risks, such as cybersecurity threats targeting model weights and training datasets. To prevent overlapping responsibilities, the chairs of the AI Governance, Audit, and Risk Committees must hold quarterly alignment meetings to review the consolidated risk register.Operational Case Study C1.4: Board Oversight of Agentic Workflows in Global Operations

In this case study, we examine the deployment of an enterprise agentic workforce at a global manufacturing firm. The Board's Value Panel demanded a 40% reduction in procurement cycle times through autonomous purchasing agents. However, the Governance Panel noted that autonomous agents lacked legal authority to bind the corporation to contracts exceeding $50,000. Under traditional governance, this project would have stalled. The dual-panel framework resolved this conflict by creating a programmatic gateway. The Value Panel defined the target cycle times and compute tags, while the Governance Panel mandated that any contract exceeding the $50,000 threshold must trigger an automated workflow pause and route to the corporate purchasing officer for approval. This system demonstrates the practical value of the Value vs. Governance Panel split, ensuring compliance without stalling innovation.The Role of the Nominating and Corporate Governance Committee in AI Talent Acquisition

Boards must evaluate if their current membership possesses the competencies required for AI oversight. The Nominating and Corporate Governance Committee is tasked with auditing board composition and identifying gaps in technical knowledge. In 2026, corporate governance standards recommend that at least one member of the board have background in artificial intelligence engineering or digital infrastructure management. If no director meets these qualifications, the board must establish an external Advisory Council to support the Value and Governance Panels. This Advisory Council provides objective audits of the management's AI strategy, model compute investments, and regulatory compliance postures.Institutional Investor Demands and Proxy Voting Guidelines

Institutional investors are increasingly voting against nominating committee chairs at companies that fail to disclose their AI governance frameworks. Glass Lewis and ISS (Institutional Shareholder Services) have published guidelines stating that companies must explain how the board oversees AI-related risks, including algorithmic bias, data privacy, and job displacement. Narrative descriptions are no longer sufficient; investors require structured metrics showing the board's engagement with risk classification systems and audit-proof ROI. The board proxy season AI disclosures flow outlined in Figure 4 provides the structured approach necessary to satisfy these requirements.Integrating AI Oversight with the Audit and Risk Committees

While the AI Governance Committee coordinates the panels, it must work closely with the Audit and Risk Committees. The Audit Committee retains responsibility for internal controls over financial reporting (ICFR), including the validation of AI-generated financial forecasts. The Risk Committee monitors systemic risks, such as cybersecurity threats targeting model weights and training datasets. To prevent overlapping responsibilities, the chairs of the AI Governance, Audit, and Risk Committees must hold quarterly alignment meetings to review the consolidated risk register.Operational Case Study C1.5: Board Oversight of Agentic Workflows in Global Operations

In this case study, we examine the deployment of an enterprise agentic workforce at a global manufacturing firm. The Board's Value Panel demanded a 40% reduction in procurement cycle times through autonomous purchasing agents. However, the Governance Panel noted that autonomous agents lacked legal authority to bind the corporation to contracts exceeding $50,000. Under traditional governance, this project would have stalled. The dual-panel framework resolved this conflict by creating a programmatic gateway. The Value Panel defined the target cycle times and compute tags, while the Governance Panel mandated that any contract exceeding the $50,000 threshold must trigger an automated workflow pause and route to the corporate purchasing officer for approval. This system demonstrates the practical value of the Value vs. Governance Panel split, ensuring compliance without stalling innovation.The Role of the Nominating and Corporate Governance Committee in AI Talent Acquisition

Boards must evaluate if their current membership possesses the competencies required for AI oversight. The Nominating and Corporate Governance Committee is tasked with auditing board composition and identifying gaps in technical knowledge. In 2026, corporate governance standards recommend that at least one member of the board have background in artificial intelligence engineering or digital infrastructure management. If no director meets these qualifications, the board must establish an external Advisory Council to support the Value and Governance Panels. This Advisory Council provides objective audits of the management's AI strategy, model compute investments, and regulatory compliance postures.Institutional Investor Demands and Proxy Voting Guidelines

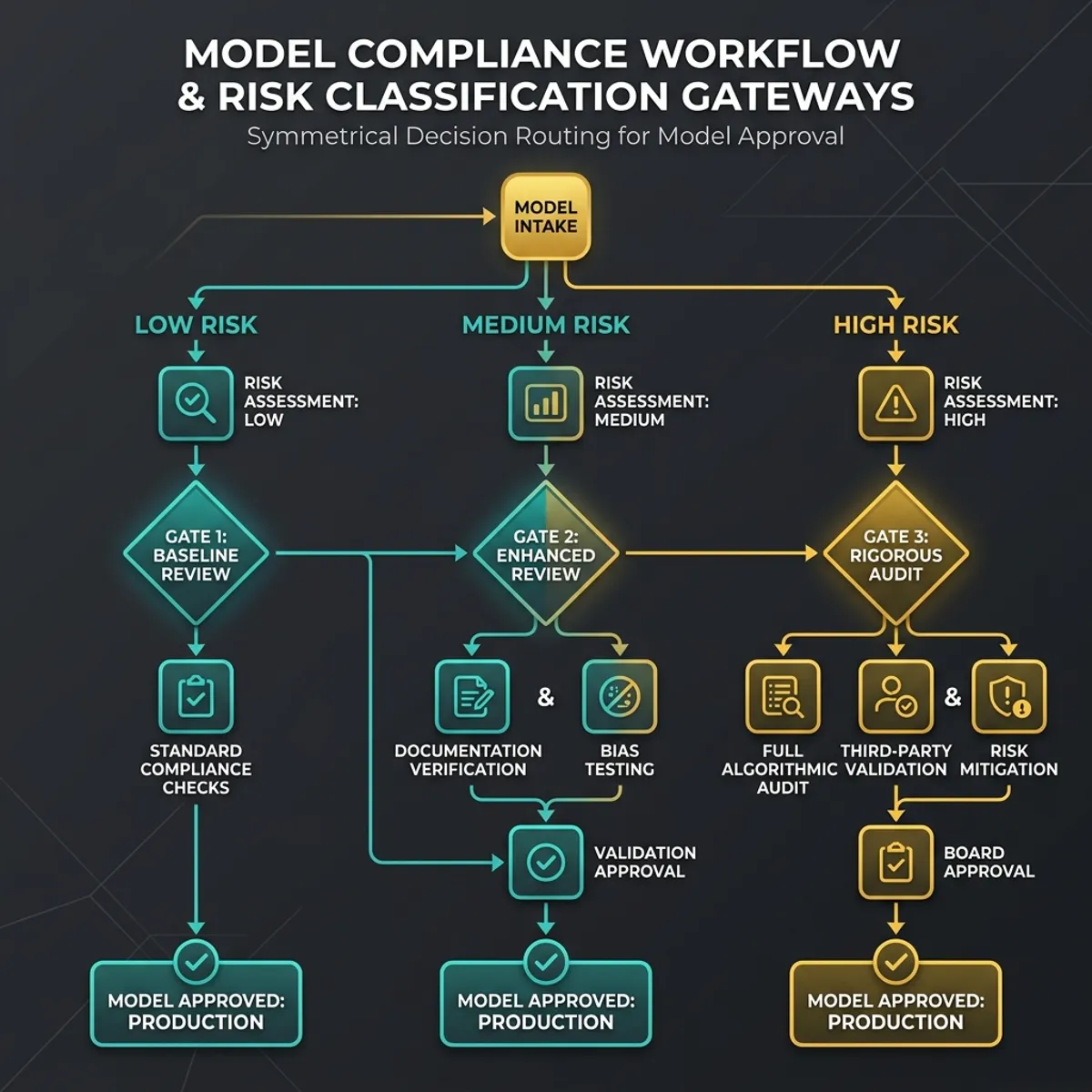

Institutional investors are increasingly voting against nominating committee chairs at companies that fail to disclose their AI governance frameworks. Glass Lewis and ISS (Institutional Shareholder Services) have published guidelines stating that companies must explain how the board oversees AI-related risks, including algorithmic bias, data privacy, and job displacement. Narrative descriptions are no longer sufficient; investors require structured metrics showing the board's engagement with risk classification systems and audit-proof ROI. The board proxy season AI disclosures flow outlined in Figure 4 provides the structured approach necessary to satisfy these requirements.Chapter 2: AI Inventory & Risk Classification (Tiers 0–4)

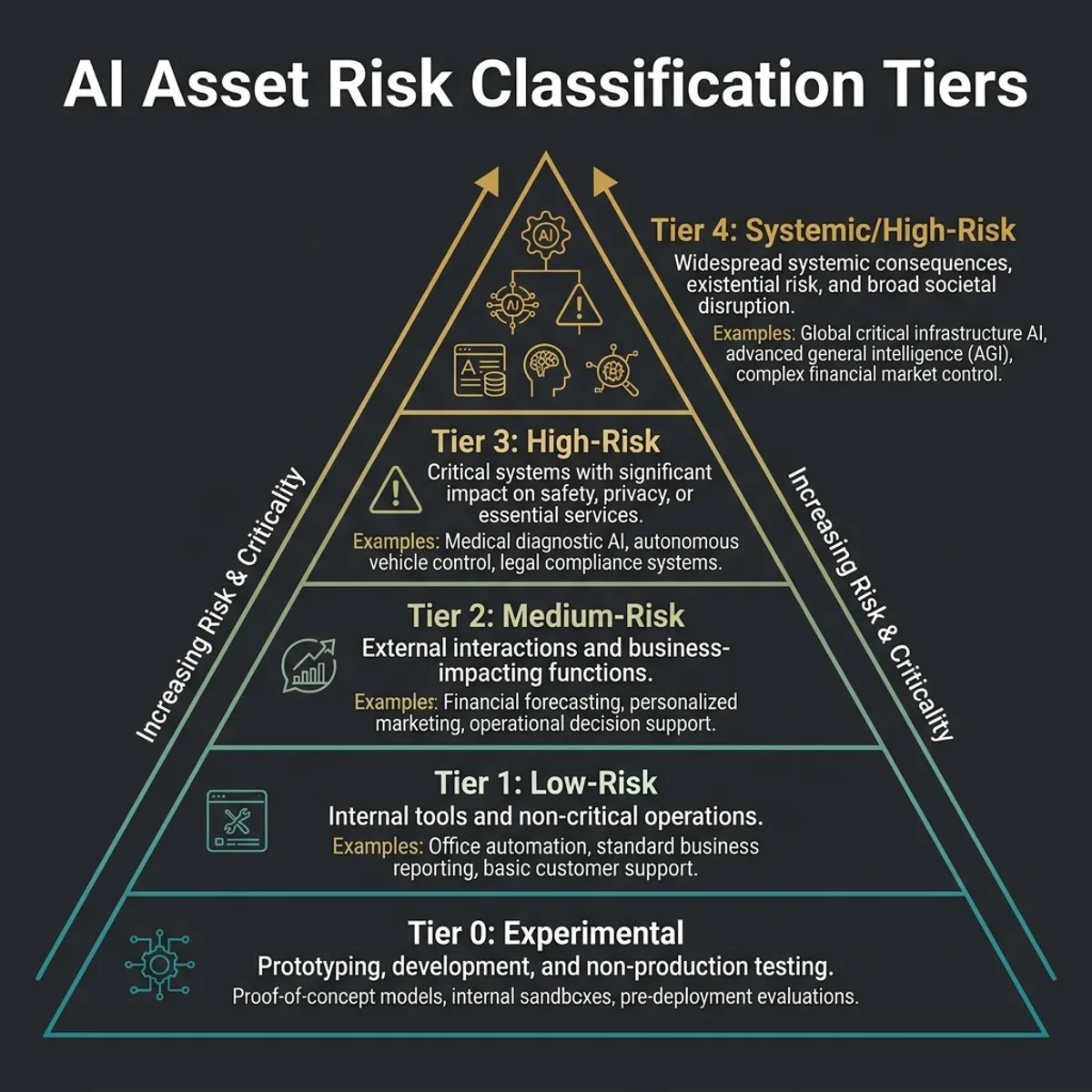

A critical failure in modern corporate governance is the lack of visibility into the corporate AI footprint. Without a unified registry of all active models, APIs, and data pipelines, boards are exposed to shadow AI—unauthorized, unmonitored tools deployed by teams seeking quick productivity hacks. To eliminate this vulnerability, the Governance Panel must mandate the creation and continuous maintenance of a Tiered AI Inventory Registry.

The Five Tiers of AI Risk

To simplify oversight and customize governance controls, all corporate AI assets must be classified into five distinct risk tiers, from T0 (Experimental/Low-risk) to T4 (Systemic/High-risk).

[Tier 4: Systemic / High-Risk] --> Direct Customer Decision, Health, Safety, Finance

|

[Tier 3: Core Operations] --> Supply Chain, Internal Financial Forecasting, HR Data

|

[Tier 2: Internal Support] --> Code generation, Internal Wiki Search, Document Parsing

|

[Tier 1: Informational] --> Static Summarizers, General Search Bots

|

[Tier 0: Experimental] --> Sandbox testing, Local offline experimentsTier 4: Systemic / High-Risk

This tier includes all systems that directly interact with customers in a high-stakes capacity, make automated decisions affecting individual livelihoods (such as credit scoring, hiring, or medical evaluations), or process highly sensitive data. Tier 4 systems are subject to strict compliance under the EU AI Act. They require continuous monitoring, regular independent third-party audits, and mandatory human-in-the-loop override systems.Tier 3: Core Operations

Tier 3 covers models that support core business processes, such as supply chain optimization algorithms, inventory forecasting, internal financial reporting engines, and human resource management analytics. A failure in a Tier 3 model could disrupt business continuity or cause material financial reporting errors, but it does not carry the same direct legal liability as a Tier 4 violation.Tier 2: Internal Support

This tier comprises tools designed to improve developer or administrative productivity, such as code assistants, internal documentation search engines, and administrative document parsing pipelines. While Tier 2 tools process proprietary company data, they are separated from external networks and do not make automated business decisions.Tier 1: Informational

Tier 1 includes general informational tools, such as static translation models, public research summarizers, and general knowledge search bots. These models do not process proprietary data or interact with core business systems, posing minimal risk.Tier 0: Experimental

Tier 0 is reserved for offline sandboxes and localized developer experimentation. These models are strictly blocked from accessing production databases or external networks. They are excluded from heavy compliance audits to encourage innovation within a secure sandbox environment.

The Programmatic Classification Gateway

To prevent subjective manual classification, all new AI projects must pass through a programmatic classification gateway before resource allocation. This gateway uses structured logic to determine the appropriate risk tier based on system inputs, data sensitivity, and operational exposure.

Below is a Python snippet illustrating how the programmatic gateway automatically assigns a risk tier and generates the compliance requirements ledger.

def classify_ai_asset(has_pii, direct_customer_action, health_safety_impact, is_offline_sandbox):

if is_offline_sandbox:

return {

"tier": "Tier 0",

"controls": ["Developer Sandbox Isolation"],

"audit_frequency_days": 360

}

if health_safety_impact or (direct_customer_action and has_pii):

return {

"tier": "Tier 4",

"controls": ["Immutable Telemetry Logging", "Human-in-the-loop Override", "Independent Third-Party Audit", "EU AI Act Compliance Registration"],

"audit_frequency_days": 90

}

if direct_customer_action or has_pii:

return {

"tier": "Tier 3",

"controls": ["Data Minimization Gateways", "Daily Bias Scans", "DPIA Documentation"],

"audit_frequency_days": 180

}

if not has_pii and not direct_customer_action:

return {

"tier": "Tier 2",

"controls": ["Internal IP Protection Filtering", "Endpoint Verification Controls"],

"audit_frequency_days": 270

}

return {

"tier": "Tier 1",

"controls": ["Standard Usage Logging"],

"audit_frequency_days": 360

}Eliminating Shadow AI with Automated Network Discovery

Manual inventory reporting is inherently prone to errors. Teams frequently bypass IT procurement to deploy external LLM endpoints for rapid tasks. The Governance Panel must mandate the integration of automated network egress scanners to intercept unauthorized API calls.

By monitoring DNS requests and HTTP traffic, the enterprise can identify undocumented outbound requests to model APIs. Any request containing payload patterns that match LLM formatting (e.g., prompt-completion pairs) is automatically intercepted and routed to the central registry for verification.

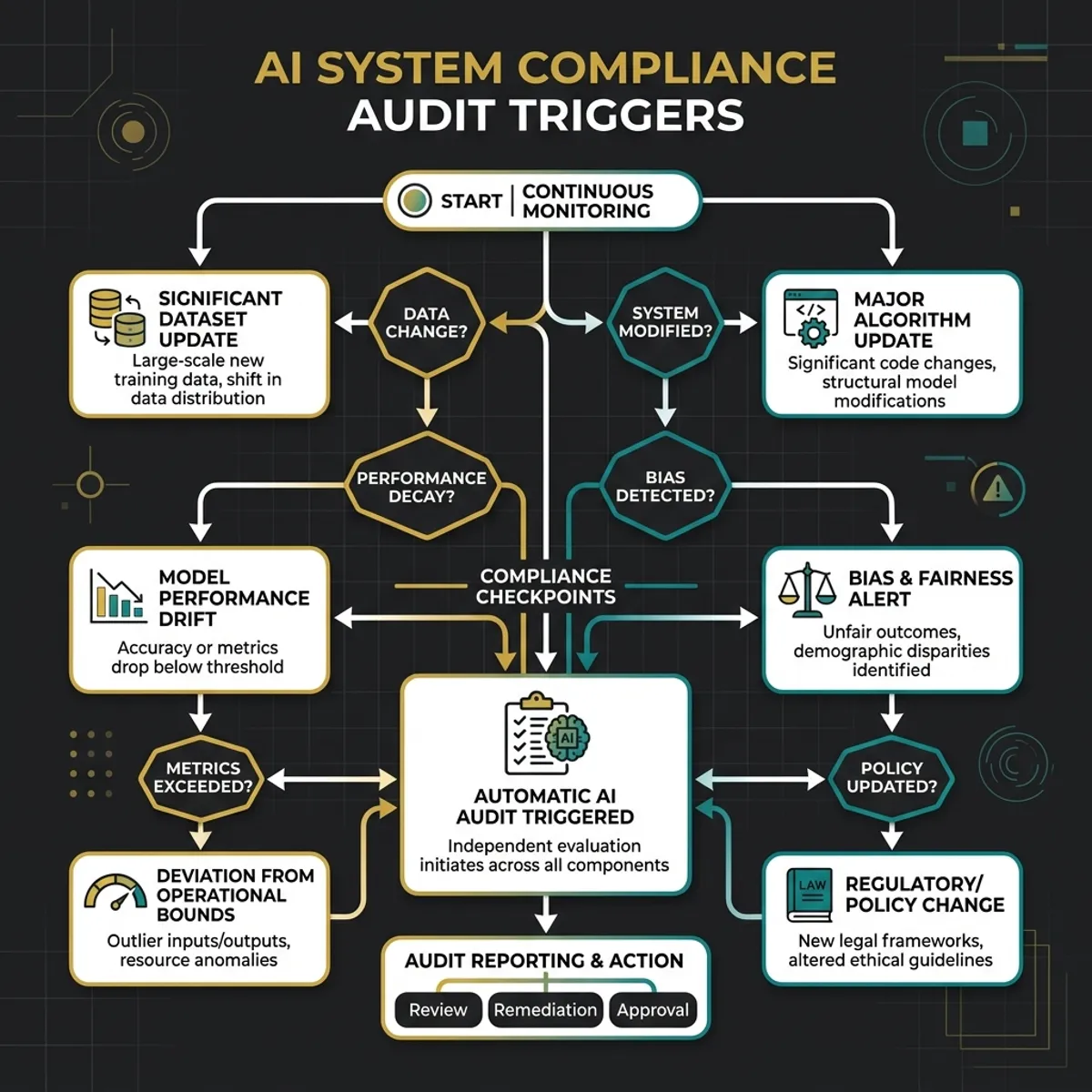

Audit Triggers and Evidence Collection

Once a model is registered, it must periodically generate verifiable audit evidence. This evidence is crucial for satisfying the audit standards of regulatory bodies and external auditors (such as ISO 42001, NIST AI RMF, and AICPA TSC AI).

This audit pipeline shows how metric drift, schema changes, or regulatory updates trigger automated evidence collection. The collected telemetry is saved to a Write-Once-Read-Many (WORM) database to ensure its integrity.

Data Protection Impact Assessments (DPIA) for AI

For all Tier 3 and Tier 4 systems, a Data Protection Impact Assessment (DPIA) must be performed and documented. The DPIA must specifically address:

- System Data Flow: A detailed map of how input prompts, training data, and generated completions flow through internal servers and external third-party APIs.

- Data Minimization: Proof that personal identifiable information (PII) is scrubbed or anonymized before transmission to the model.

- Model Memorization and Leakage: Vulnerability assessments confirming that the model cannot be coerced into revealing sensitive training data through prompt injection attacks.

- Third-Party Data Policies: Verification of the data retention and model training policies of all third-party API providers utilized by the system.

Regulatory Deep Dive C2.1: Aligning with the EU AI Act and NIST AI RMF

Under the EU AI Act, systems classified as 'High-Risk' must comply with strict obligations before they can be placed on the European market. These obligations include establishing a risk management system, performing detailed data governance audits, and ensuring high levels of cybersecurity. The Governance Panel must verify that the company’s Tier 4 models satisfy these mandates. This requires implementing continuous logging of model inputs and outputs, providing clear instructions for human operators, and establishing a post-market monitoring plan. The NIST AI Risk Management Framework (NIST AI RMF 1.0) provides a complementary set of guidelines for mapping, measuring, managing, and governing AI risks in non-European jurisdictions.Eliminating Shadow AI: Network Security and API Governance

Shadow AI represents a major security vulnerability for modern enterprises. When employees copy proprietary source code or customer data into public, unmanaged LLM interfaces, the company loses custody of its intellectual property. To eliminate this risk, the IT department must deploy network security tools that scan outbound traffic for unauthorized API calls to known AI providers. Any traffic matching these patterns is blocked, and the user is redirected to the company's approved API gateway. This gateway enforces data protection filters, logs all requests for audit purposes, and maps compute costs to the appropriate business unit.Implementing Data Protection Impact Assessments (DPIA) for Multi-Modal Models

Multi-modal models—which process text, images, and audio—require specialized Data Protection Impact Assessments. The data protection officer must evaluate how the system handles biometric data, voice recordings, and images of individuals. For example, if an AI customer service agent records voice calls to analyze customer sentiment, this data is classified as biometric under the GDPR and requires explicit customer consent. The DPIA must document the technical controls used to encrypt, anonymize, and delete these recordings after processing, ensuring compliance with global privacy regulations.Vulnerability Management: Prompt Injection and Model Poisoning

Traditional software vulnerability scanners are ineffective against AI models. The Governance Panel must mandate regular red-teaming exercises to test the resilience of production models against prompt injection attacks, where a user inputs malicious text designed to bypass the model's safety guardrails. Additionally, the data pipeline team must audit all training datasets to prevent data poisoning, where a malicious actor alters training data to create a backdoor in the model. These vulnerability reports must be reviewed by the Governance Panel during quarterly audits.Regulatory Deep Dive C2.2: Aligning with the EU AI Act and NIST AI RMF

Under the EU AI Act, systems classified as 'High-Risk' must comply with strict obligations before they can be placed on the European market. These obligations include establishing a risk management system, performing detailed data governance audits, and ensuring high levels of cybersecurity. The Governance Panel must verify that the company’s Tier 4 models satisfy these mandates. This requires implementing continuous logging of model inputs and outputs, providing clear instructions for human operators, and establishing a post-market monitoring plan. The NIST AI Risk Management Framework (NIST AI RMF 1.0) provides a complementary set of guidelines for mapping, measuring, managing, and governing AI risks in non-European jurisdictions.Eliminating Shadow AI: Network Security and API Governance

Shadow AI represents a major security vulnerability for modern enterprises. When employees copy proprietary source code or customer data into public, unmanaged LLM interfaces, the company loses custody of its intellectual property. To eliminate this risk, the IT department must deploy network security tools that scan outbound traffic for unauthorized API calls to known AI providers. Any traffic matching these patterns is blocked, and the user is redirected to the company's approved API gateway. This gateway enforces data protection filters, logs all requests for audit purposes, and maps compute costs to the appropriate business unit.Implementing Data Protection Impact Assessments (DPIA) for Multi-Modal Models

Multi-modal models—which process text, images, and audio—require specialized Data Protection Impact Assessments. The data protection officer must evaluate how the system handles biometric data, voice recordings, and images of individuals. For example, if an AI customer service agent records voice calls to analyze customer sentiment, this data is classified as biometric under the GDPR and requires explicit customer consent. The DPIA must document the technical controls used to encrypt, anonymize, and delete these recordings after processing, ensuring compliance with global privacy regulations.Vulnerability Management: Prompt Injection and Model Poisoning

Traditional software vulnerability scanners are ineffective against AI models. The Governance Panel must mandate regular red-teaming exercises to test the resilience of production models against prompt injection attacks, where a user inputs malicious text designed to bypass the model's safety guardrails. Additionally, the data pipeline team must audit all training datasets to prevent data poisoning, where a malicious actor alters training data to create a backdoor in the model. These vulnerability reports must be reviewed by the Governance Panel during quarterly audits.Regulatory Deep Dive C2.3: Aligning with the EU AI Act and NIST AI RMF

Under the EU AI Act, systems classified as 'High-Risk' must comply with strict obligations before they can be placed on the European market. These obligations include establishing a risk management system, performing detailed data governance audits, and ensuring high levels of cybersecurity. The Governance Panel must verify that the company’s Tier 4 models satisfy these mandates. This requires implementing continuous logging of model inputs and outputs, providing clear instructions for human operators, and establishing a post-market monitoring plan. The NIST AI Risk Management Framework (NIST AI RMF 1.0) provides a complementary set of guidelines for mapping, measuring, managing, and governing AI risks in non-European jurisdictions.Eliminating Shadow AI: Network Security and API Governance

Shadow AI represents a major security vulnerability for modern enterprises. When employees copy proprietary source code or customer data into public, unmanaged LLM interfaces, the company loses custody of its intellectual property. To eliminate this risk, the IT department must deploy network security tools that scan outbound traffic for unauthorized API calls to known AI providers. Any traffic matching these patterns is blocked, and the user is redirected to the company's approved API gateway. This gateway enforces data protection filters, logs all requests for audit purposes, and maps compute costs to the appropriate business unit.Implementing Data Protection Impact Assessments (DPIA) for Multi-Modal Models

Multi-modal models—which process text, images, and audio—require specialized Data Protection Impact Assessments. The data protection officer must evaluate how the system handles biometric data, voice recordings, and images of individuals. For example, if an AI customer service agent records voice calls to analyze customer sentiment, this data is classified as biometric under the GDPR and requires explicit customer consent. The DPIA must document the technical controls used to encrypt, anonymize, and delete these recordings after processing, ensuring compliance with global privacy regulations.Vulnerability Management: Prompt Injection and Model Poisoning

Traditional software vulnerability scanners are ineffective against AI models. The Governance Panel must mandate regular red-teaming exercises to test the resilience of production models against prompt injection attacks, where a user inputs malicious text designed to bypass the model's safety guardrails. Additionally, the data pipeline team must audit all training datasets to prevent data poisoning, where a malicious actor alters training data to create a backdoor in the model. These vulnerability reports must be reviewed by the Governance Panel during quarterly audits.Regulatory Deep Dive C2.4: Aligning with the EU AI Act and NIST AI RMF

Under the EU AI Act, systems classified as 'High-Risk' must comply with strict obligations before they can be placed on the European market. These obligations include establishing a risk management system, performing detailed data governance audits, and ensuring high levels of cybersecurity. The Governance Panel must verify that the company’s Tier 4 models satisfy these mandates. This requires implementing continuous logging of model inputs and outputs, providing clear instructions for human operators, and establishing a post-market monitoring plan. The NIST AI Risk Management Framework (NIST AI RMF 1.0) provides a complementary set of guidelines for mapping, measuring, managing, and governing AI risks in non-European jurisdictions.Eliminating Shadow AI: Network Security and API Governance

Shadow AI represents a major security vulnerability for modern enterprises. When employees copy proprietary source code or customer data into public, unmanaged LLM interfaces, the company loses custody of its intellectual property. To eliminate this risk, the IT department must deploy network security tools that scan outbound traffic for unauthorized API calls to known AI providers. Any traffic matching these patterns is blocked, and the user is redirected to the company's approved API gateway. This gateway enforces data protection filters, logs all requests for audit purposes, and maps compute costs to the appropriate business unit.Implementing Data Protection Impact Assessments (DPIA) for Multi-Modal Models

Multi-modal models—which process text, images, and audio—require specialized Data Protection Impact Assessments. The data protection officer must evaluate how the system handles biometric data, voice recordings, and images of individuals. For example, if an AI customer service agent records voice calls to analyze customer sentiment, this data is classified as biometric under the GDPR and requires explicit customer consent. The DPIA must document the technical controls used to encrypt, anonymize, and delete these recordings after processing, ensuring compliance with global privacy regulations.Vulnerability Management: Prompt Injection and Model Poisoning

Traditional software vulnerability scanners are ineffective against AI models. The Governance Panel must mandate regular red-teaming exercises to test the resilience of production models against prompt injection attacks, where a user inputs malicious text designed to bypass the model's safety guardrails. Additionally, the data pipeline team must audit all training datasets to prevent data poisoning, where a malicious actor alters training data to create a backdoor in the model. These vulnerability reports must be reviewed by the Governance Panel during quarterly audits.Regulatory Deep Dive C2.5: Aligning with the EU AI Act and NIST AI RMF

Under the EU AI Act, systems classified as 'High-Risk' must comply with strict obligations before they can be placed on the European market. These obligations include establishing a risk management system, performing detailed data governance audits, and ensuring high levels of cybersecurity. The Governance Panel must verify that the company’s Tier 4 models satisfy these mandates. This requires implementing continuous logging of model inputs and outputs, providing clear instructions for human operators, and establishing a post-market monitoring plan. The NIST AI Risk Management Framework (NIST AI RMF 1.0) provides a complementary set of guidelines for mapping, measuring, managing, and governing AI risks in non-European jurisdictions.Eliminating Shadow AI: Network Security and API Governance

Shadow AI represents a major security vulnerability for modern enterprises. When employees copy proprietary source code or customer data into public, unmanaged LLM interfaces, the company loses custody of its intellectual property. To eliminate this risk, the IT department must deploy network security tools that scan outbound traffic for unauthorized API calls to known AI providers. Any traffic matching these patterns is blocked, and the user is redirected to the company's approved API gateway. This gateway enforces data protection filters, logs all requests for audit purposes, and maps compute costs to the appropriate business unit.Implementing Data Protection Impact Assessments (DPIA) for Multi-Modal Models

Multi-modal models—which process text, images, and audio—require specialized Data Protection Impact Assessments. The data protection officer must evaluate how the system handles biometric data, voice recordings, and images of individuals. For example, if an AI customer service agent records voice calls to analyze customer sentiment, this data is classified as biometric under the GDPR and requires explicit customer consent. The DPIA must document the technical controls used to encrypt, anonymize, and delete these recordings after processing, ensuring compliance with global privacy regulations.Chapter 3: ROI Metrics That Survive Audit

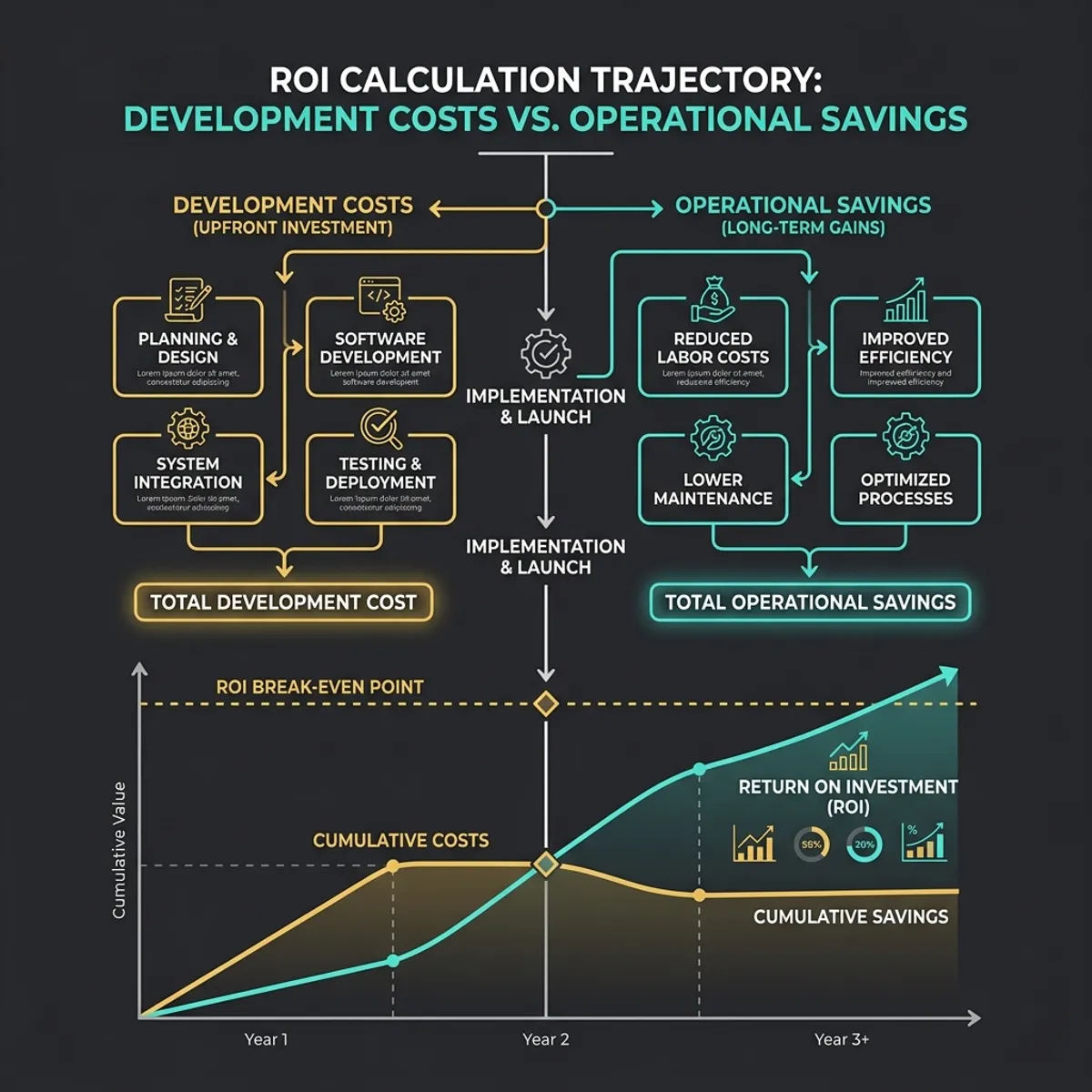

The biggest challenge facing boards when evaluating AI programs is the lack of standardized, audit-proof ROI methodologies. Technology leaders often report "soft metrics," such as "hours saved" or "user adoption rates." While useful for engineering teams, these metrics do not translate to financial statements. To enforce capital allocation discipline, the Value Panel must establish a metrics framework that external auditors can validate.

The Standard AI ROI Equation

To measure the financial return on AI systems, the board must evaluate the net margin impact against the fully loaded cost of compute, human oversight, and implementation.

$$\text{AI ROI} = \frac{\text{Net Financial Offsets} - \text{Amortized Cost of Development and Compute}}{\text{Amortized Cost of Development and Compute}}$$

Where:

- Net Financial Offsets represents the sum of digital labor savings, productivity gains that translate to lower hiring needs, and incremental revenue directly generated by the AI system.

- Cost of Development and Compute includes developer salaries, model API token costs, compute infrastructure depreciation, licensing fees, and compliance audit costs.

Digital Labor Offsets and Productivity Multipliers

To calculate labor productivity gains accurately, the board must use a digital labor offset model. Instead of asking employees to estimate their saved time, the company must instrument its workflow tools to measure the actual reduction in task completion times.

Total Hours Saved = (Baseline Task Completion Time - AI Task Completion Time) x Volume of Tasks

Digital Labor Value = Total Hours Saved x Hourly Fully Loaded Compensation Rate of Target RoleHowever, these hours saved only contribute to the bottom line if the organization either reduces its headcount, redirects the saved hours to higher-value activities that generate incremental revenue, or reduces external contractor expenditures. If the saved hours are merely spent on administrative overhead, the realized ROI is zero.

Amortizing Model Compute and Compute Costs

A common mistake in AI accounting is treating large training runs as immediate operating expenses. Training a proprietary model on corporate datasets creates a long-term intangible asset. Therefore, training costs must be capitalized and amortized over the expected shelf-life of the model (typically 12 to 24 months, given the rapid rate of obsolescence).

Conversely, inference costs—the recurring API fees or GPU cycles spent running the model in production—must be treated as cost of goods sold (COGS) or operating expenses (OpEx) depending on whether the model directly serves customers or supports internal teams.

Below is an operational ledger structure designed to track model resource amortization and calculate net margins by business value lane.

{

"model_depreciation_ledger": {

"model_id": "model_customer_support_v2",

"training_cost": 240000.00,

"capitalization_date": "2026-01-15",

"useful_life_months": 12,

"monthly_amortization": 20000.00,

"inference_cogs_per_call": 0.004,

"associated_business_unit": "Global Customer Support"

}

}Capital Allocation Discipline: The Hurdle Rate Framework

The Value Panel must establish clear financial thresholds (hurdle rates) for all AI projects based on their risk tier. Because of the high risk of technological obsolescence, AI projects must achieve a higher return on investment than standard enterprise software deployments.

The Value Panel enforces these hurdle rates during the capital budgeting process, ensuring that speculative projects are not funded at the expense of high-yield core improvements.

Key Performance Indicators (KPIs) for the Value Panel

Below is the standard dashboard matrix of KPIs that the Value Panel must review quarterly to evaluate portfolio performance:

| Metric Name | Calculation Method | Target Threshold | Validation Method |

|---|---|---|---|

| Compute Efficiency Ratio (CER) | Total realized margin impact / Total compute token spend | > 3.5x | FinOps ledger tags matched to margin improvements |

| Digital Labor Margin (DLM) | (FTE labor offsets - inference costs) / FTE labor offsets | > 70% | HR headcount trends compared with API log volumes |

| Model Obsolescence Rate (MOR) | Time from deployment to next model iteration | > 9 Months | Registry entry updates and deprecation logs |

| Compute Unit Cost (CUC) | Inference cost per 1M tokens by model family | < $1.20 | Vendor invoices and internal GPU telemetry logs |

By establishing these metrics, the board can protect the enterprise from "AI greenwashing" by executives, ensuring that every dollar invested in technology yields measurable returns. In the next chapter, we will address the incident response protocols and audit ledgers necessary to manage operational failures and model drift.

Financial Analysis C3.1: FinOps Tagging and Cost Optimization

Implementing FinOps tagging is essential for tracking the compute cost of AI applications. Every API call, database query, and model training run must be tagged with metadata indicating the project ID, business unit, and risk tier. This allows the finance team to attribute compute expenditures to specific business units and calculate the cost of goods sold (COGS) for each application. For example, if the marketing department deploys a product description generator, the API token costs are charged directly to marketing’s budget. The Value Panel reviews these cost reports monthly to identify inefficient systems that are failing to meet their ROI hurdle rates.Measuring the Productivity Multiplier of Developer Assistants

Developer assistants (such as GitHub Copilot or internal code generators) are often cited as high-yielding AI investments. However, measuring their actual financial impact is challenging. The engineering team must track objective productivity metrics, such as pull request cycle times, code review defect rates, and the volume of code committed per developer. If these assistants improve developer throughput by 20%, the organization can handle more development tasks in-house or reduce its reliance on external engineering contractors. The Value Panel must verify that these productivity gains translate directly to lower software development costs on the income statement.Capitalizing vs. Expensing AI R&D Costs

Under GAAP and IFRS accounting standards, companies must carefully classify AI research and development costs. Pre-development activities, such as exploratory feasibility studies and model evaluation, must be expensed as incurred. However, once the technical feasibility of the system is established, the development costs (including developer salaries and compute training run costs) can be capitalized as intangible assets. These assets are then amortized over their useful life, reducing the immediate impact on operating margins and providing a more accurate representation of the company’s capital investments.The Amortization Schedule of Proprietary Foundation Models

When a company trains a proprietary foundation model, it represents a multi-million dollar capital expenditure. The useful life of these models is highly compressed due to the rapid pace of technological innovation. A model trained in 2026 may be obsolete by 2027 as more efficient architectures emerge. The Value Panel must enforce a conservative amortization schedule, depreciating the model asset over a maximum of 12 months. This conservative approach prevents the company from carrying overvalued, obsolete technology assets on its balance sheet.Financial Analysis C3.2: FinOps Tagging and Cost Optimization

Implementing FinOps tagging is essential for tracking the compute cost of AI applications. Every API call, database query, and model training run must be tagged with metadata indicating the project ID, business unit, and risk tier. This allows the finance team to attribute compute expenditures to specific business units and calculate the cost of goods sold (COGS) for each application. For example, if the marketing department deploys a product description generator, the API token costs are charged directly to marketing’s budget. The Value Panel reviews these cost reports monthly to identify inefficient systems that are failing to meet their ROI hurdle rates.Measuring the Productivity Multiplier of Developer Assistants

Developer assistants (such as GitHub Copilot or internal code generators) are often cited as high-yielding AI investments. However, measuring their actual financial impact is challenging. The engineering team must track objective productivity metrics, such as pull request cycle times, code review defect rates, and the volume of code committed per developer. If these assistants improve developer throughput by 20%, the organization can handle more development tasks in-house or reduce its reliance on external engineering contractors. The Value Panel must verify that these productivity gains translate directly to lower software development costs on the income statement.Capitalizing vs. Expensing AI R&D Costs

Under GAAP and IFRS accounting standards, companies must carefully classify AI research and development costs. Pre-development activities, such as exploratory feasibility studies and model evaluation, must be expensed as incurred. However, once the technical feasibility of the system is established, the development costs (including developer salaries and compute training run costs) can be capitalized as intangible assets. These assets are then amortized over their useful life, reducing the immediate impact on operating margins and providing a more accurate representation of the company’s capital investments.The Amortization Schedule of Proprietary Foundation Models

When a company trains a proprietary foundation model, it represents a multi-million dollar capital expenditure. The useful life of these models is highly compressed due to the rapid pace of technological innovation. A model trained in 2026 may be obsolete by 2027 as more efficient architectures emerge. The Value Panel must enforce a conservative amortization schedule, depreciating the model asset over a maximum of 12 months. This conservative approach prevents the company from carrying overvalued, obsolete technology assets on its balance sheet.Financial Analysis C3.3: FinOps Tagging and Cost Optimization

Implementing FinOps tagging is essential for tracking the compute cost of AI applications. Every API call, database query, and model training run must be tagged with metadata indicating the project ID, business unit, and risk tier. This allows the finance team to attribute compute expenditures to specific business units and calculate the cost of goods sold (COGS) for each application. For example, if the marketing department deploys a product description generator, the API token costs are charged directly to marketing’s budget. The Value Panel reviews these cost reports monthly to identify inefficient systems that are failing to meet their ROI hurdle rates.Measuring the Productivity Multiplier of Developer Assistants

Developer assistants (such as GitHub Copilot or internal code generators) are often cited as high-yielding AI investments. However, measuring their actual financial impact is challenging. The engineering team must track objective productivity metrics, such as pull request cycle times, code review defect rates, and the volume of code committed per developer. If these assistants improve developer throughput by 20%, the organization can handle more development tasks in-house or reduce its reliance on external engineering contractors. The Value Panel must verify that these productivity gains translate directly to lower software development costs on the income statement.Capitalizing vs. Expensing AI R&D Costs

Under GAAP and IFRS accounting standards, companies must carefully classify AI research and development costs. Pre-development activities, such as exploratory feasibility studies and model evaluation, must be expensed as incurred. However, once the technical feasibility of the system is established, the development costs (including developer salaries and compute training run costs) can be capitalized as intangible assets. These assets are then amortized over their useful life, reducing the immediate impact on operating margins and providing a more accurate representation of the company’s capital investments.The Amortization Schedule of Proprietary Foundation Models

When a company trains a proprietary foundation model, it represents a multi-million dollar capital expenditure. The useful life of these models is highly compressed due to the rapid pace of technological innovation. A model trained in 2026 may be obsolete by 2027 as more efficient architectures emerge. The Value Panel must enforce a conservative amortization schedule, depreciating the model asset over a maximum of 12 months. This conservative approach prevents the company from carrying overvalued, obsolete technology assets on its balance sheet.Financial Analysis C3.4: FinOps Tagging and Cost Optimization

Implementing FinOps tagging is essential for tracking the compute cost of AI applications. Every API call, database query, and model training run must be tagged with metadata indicating the project ID, business unit, and risk tier. This allows the finance team to attribute compute expenditures to specific business units and calculate the cost of goods sold (COGS) for each application. For example, if the marketing department deploys a product description generator, the API token costs are charged directly to marketing’s budget. The Value Panel reviews these cost reports monthly to identify inefficient systems that are failing to meet their ROI hurdle rates.Measuring the Productivity Multiplier of Developer Assistants

Developer assistants (such as GitHub Copilot or internal code generators) are often cited as high-yielding AI investments. However, measuring their actual financial impact is challenging. The engineering team must track objective productivity metrics, such as pull request cycle times, code review defect rates, and the volume of code committed per developer. If these assistants improve developer throughput by 20%, the organization can handle more development tasks in-house or reduce its reliance on external engineering contractors. The Value Panel must verify that these productivity gains translate directly to lower software development costs on the income statement.Capitalizing vs. Expensing AI R&D Costs

Under GAAP and IFRS accounting standards, companies must carefully classify AI research and development costs. Pre-development activities, such as exploratory feasibility studies and model evaluation, must be expensed as incurred. However, once the technical feasibility of the system is established, the development costs (including developer salaries and compute training run costs) can be capitalized as intangible assets. These assets are then amortized over their useful life, reducing the immediate impact on operating margins and providing a more accurate representation of the company’s capital investments.The Amortization Schedule of Proprietary Foundation Models

When a company trains a proprietary foundation model, it represents a multi-million dollar capital expenditure. The useful life of these models is highly compressed due to the rapid pace of technological innovation. A model trained in 2026 may be obsolete by 2027 as more efficient architectures emerge. The Value Panel must enforce a conservative amortization schedule, depreciating the model asset over a maximum of 12 months. This conservative approach prevents the company from carrying overvalued, obsolete technology assets on its balance sheet.Financial Analysis C3.5: FinOps Tagging and Cost Optimization

Implementing FinOps tagging is essential for tracking the compute cost of AI applications. Every API call, database query, and model training run must be tagged with metadata indicating the project ID, business unit, and risk tier. This allows the finance team to attribute compute expenditures to specific business units and calculate the cost of goods sold (COGS) for each application. For example, if the marketing department deploys a product description generator, the API token costs are charged directly to marketing’s budget. The Value Panel reviews these cost reports monthly to identify inefficient systems that are failing to meet their ROI hurdle rates.Measuring the Productivity Multiplier of Developer Assistants

Developer assistants (such as GitHub Copilot or internal code generators) are often cited as high-yielding AI investments. However, measuring their actual financial impact is challenging. The engineering team must track objective productivity metrics, such as pull request cycle times, code review defect rates, and the volume of code committed per developer. If these assistants improve developer throughput by 20%, the organization can handle more development tasks in-house or reduce its reliance on external engineering contractors. The Value Panel must verify that these productivity gains translate directly to lower software development costs on the income statement.Capitalizing vs. Expensing AI R&D Costs

Under GAAP and IFRS accounting standards, companies must carefully classify AI research and development costs. Pre-development activities, such as exploratory feasibility studies and model evaluation, must be expensed as incurred. However, once the technical feasibility of the system is established, the development costs (including developer salaries and compute training run costs) can be capitalized as intangible assets. These assets are then amortized over their useful life, reducing the immediate impact on operating margins and providing a more accurate representation of the company’s capital investments.Chapter 4: Incident, Drift, Override, and Remediation Reporting

Even the most thoroughly tested AI models will eventually fail. The complex, non-deterministic nature of deep learning means that models can experience silent failure modes, including model drift, data poisoning, and adversarial prompt injections. To protect the enterprise from financial loss and reputational damage, the Governance Panel must establish a structured, automated incident escalation and remediation protocol.

Model Drift and Automated Testing Triggers

Model drift occurs when the statistical properties of the incoming production data drift away from the data used to train the model. This leads to a steady decline in model accuracy. To counter this, the engineering team must configure automated drift detectors that constantly evaluate output distributions.

$$\text{Population Stability Index (PSI)} = \sum \left( (\text{Actual}\% - \text{Expected}\%) \times \ln\left(\frac{\text{Actual}\%}{\text{Expected}\%}\right) \right)$$

When the PSI exceeds 0.2, the system automatically triggers a model drift warning. If the drift persists or increases, the model is flagged for remediation, and the incident is entered into the corporate governance log.

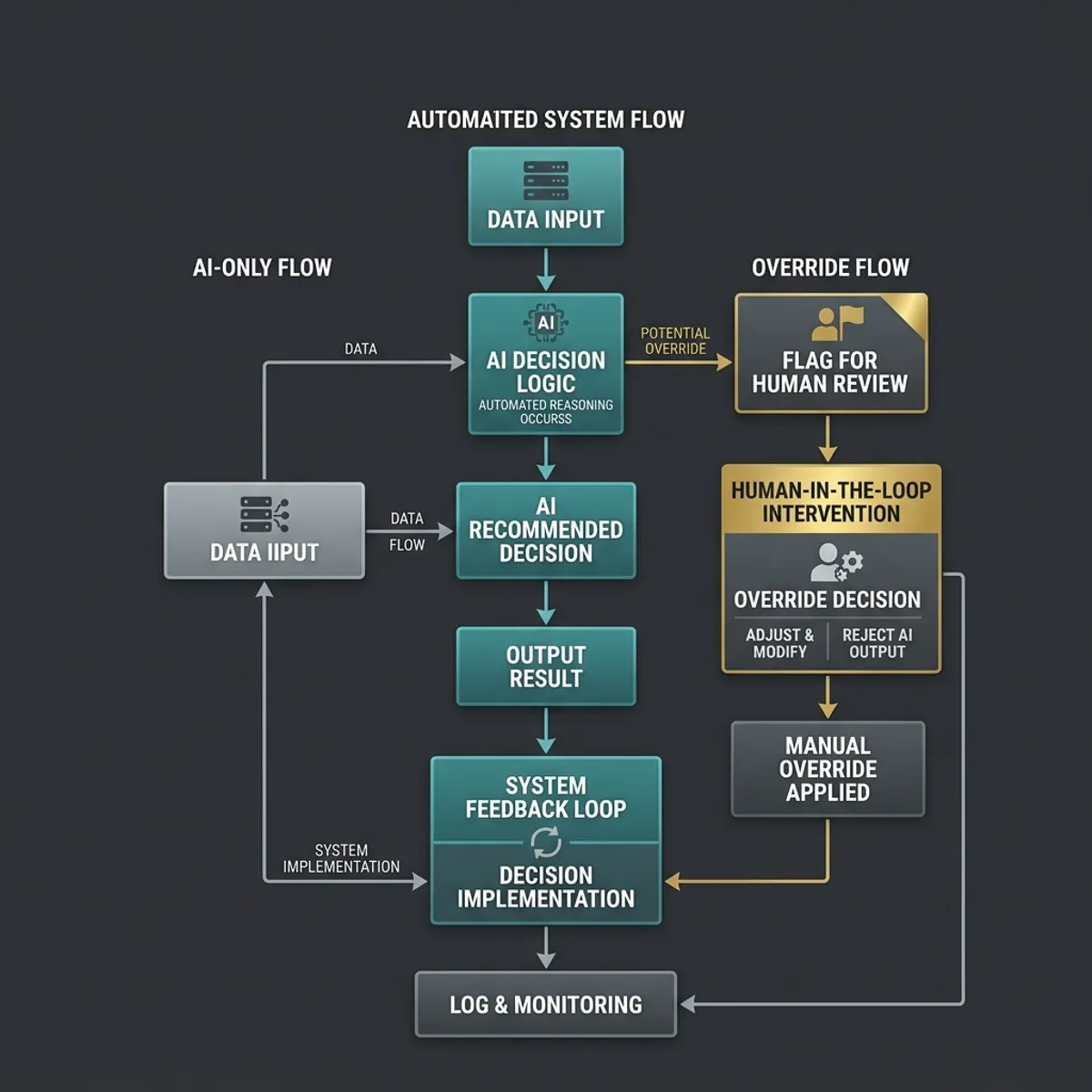

The Human-in-the-Loop Override Trace

For all Tier 4 (Systemic) and Tier 3 (Core Operational) systems, the board must mandate a human-in-the-loop override mechanism. If the automated model outputs flag an anomaly or cross a risk threshold, the action is paused until a qualified human operator reviews and approves the decision.

This override flow guarantees that a human operator is inserted into the decision path when risk levels escalate. Crucially, the system must record an immutable trace of the override—detailing who authorized the decision, why the model's recommendation was bypassed, and what data supported the human decision.

The Immutable WORM Registry for Drift and Overrides

To ensure auditability and prevent tampering, all model overrides, drift warnings, and severity escalations must be written to an immutable Write-Once-Read-Many (WORM) registry. This database is cryptographically signed and stored in a decentralized or write-blocked cloud bucket, preventing anyone—including system administrators—from deleting or modifying historical incident data.

This drift alert loop shows how production monitoring, automated triggers, and the immutable ledger operate in sync to resolve model anomalies before they impact business operations.

{

"incident_log_entry": {

"timestamp": "2026-06-14T20:15:32Z",

"incident_id": "INC-88392-AX",

"model_id": "model_credit_score_v4",

"trigger_type": "Model Drift (PSI = 0.28)",

"action_taken": "Automated fallback to Tier 3 linear model",

"operator_id": "OP-9831",

"override_justification": "Model flagged user credit score anomaly due to sudden macro-market shift; human operator verified customer credentials manually.",

"cryptographic_signature": "sha256:8f3c8a9e0f3b8c7e9d8f7e6d5c4b3a2"

}

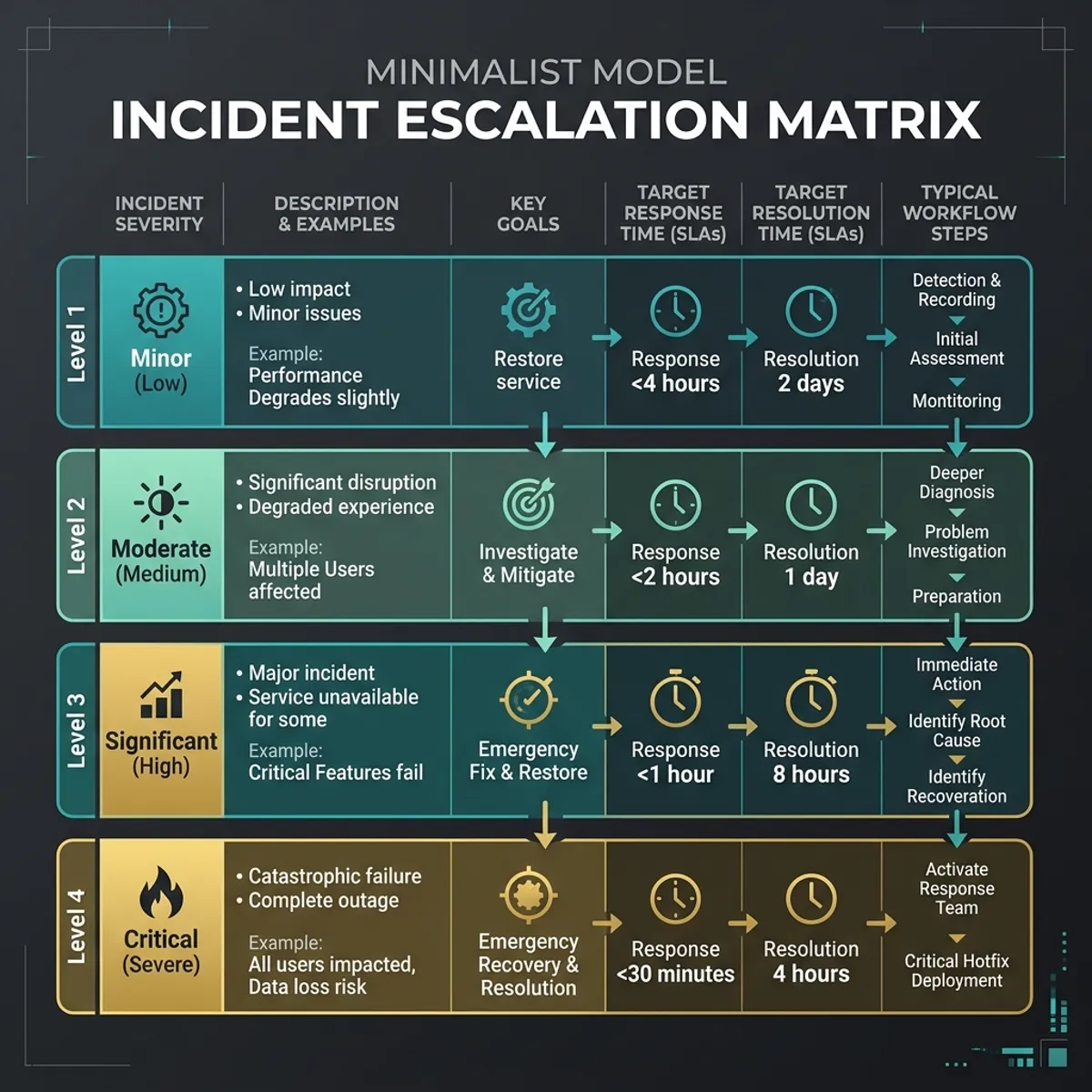

}The Incident Response and Escalation Matrix

The Governance Panel must enforce a strict timeline for incident reporting based on the severity of the operational failure. Below is the mandatory escalation matrix:

This schema outlines how operational logs, developer actions, and system responses are mapped to the audit trail to maintain compliance. The details of the response timeline are codified in the table below:

| Severity Level | Description | Escalation Path | Resolution Timeline |

|---|---|---|---|

| Critical (Level 1) | Systemic failure of a Tier 4 model, suspected data breach, or regulatory non-compliance hazard. | CISO, Chief Risk Officer, and Board Governance Panel notified within 4 hours. | Immediate rollback or patch within 12 hours. |

| High (Level 2) | Persistent model drift on a Tier 3 model or high frequency of human overrides. | CTO and Risk Management Committee notified within 24 hours. | Model retraining and deployment within 48 hours. |

| Moderate (Level 3) | Minor schema drifts, data ingestion pipeline anomalies, or slight performance dips in Tier 2 tools. | Engineering Lead notified. Summary included in monthly report. | Resolution within 5 business days. |

| Low (Level 4) | Informational anomalies or sandbox environment failures. | None. Logged locally in standard telemetry. | Addressed during regular maintenance cycles. |

Adhering to this matrix ensures that the board is not overwhelmed by minor operational alerts, while guarantees that systemic failures are escalated to directors immediately. In the final chapter, we will outline the 2026–2030 maturity runway to guide the company's long-term AI strategy.

Incident Response C4.1: Mitigating Bias and Toxicity in Customer-Facing Systems

When a customer-facing customer support model generates biased or toxic completions, the company faces immediate reputational and legal risks. The Governance Panel must ensure that all customer-facing systems utilize real-time toxicity filters that analyze the model’s outputs before they are displayed to the user. If the filter detects toxic content or policy violations, the system blocks the completion, returns a standardized fallback response, and triggers a Level 1 incident. The incident response team must then audit the model’s prompts and parameters to identify the source of the failure.Managing Model Drift in Financial Underwriting Systems

In financial underwriting systems, minor model drift can result in substantial loan default losses or regulatory violations. The risk management team must continuously compare the distribution of credit scores generated by the production model against the training baseline. If the Population Stability Index (PSI) flags a statistical drift, the system must automatically route underwriting decisions to human loan officers for manual review. The model is then scheduled for retraining on the new dataset, and the performance outcomes are documented in the immutable WORM registry.Audit Trails for Human-in-the-Loop Override Actions

The Governance Panel requires a complete audit trail for all human-in-the-loop overrides. When an operator overrides a model’s decision (such as approving a transaction that the model flagged as fraudulent), the system must prompt the operator to select a predefined justification code and input detailed comments. The operator’s ID, the model’s original output, the override action, and the justification are signed with a cryptographic hash and written to the WORM database. This audit trail is reviewed by external auditors during ISO 42001 certification reviews.Post-Incident Remediation and Lessons Learned

Following any Level 1 or Level 2 incident, the engineering and risk teams must conduct a formal post-incident review. The review must document:- Root Cause Analysis: The underlying technical failure that caused the incident (e.g., training data contamination, unhandled edge cases in user prompts).

- Impact Assessment: The financial, legal, and reputational damage caused by the incident.

- Remediation Steps: The actions taken to resolve the immediate issue and prevent future occurrences.

- Governance Updates: Recommendations for modifying the risk classification registry or updating safety policies.

Incident Response C4.2: Mitigating Bias and Toxicity in Customer-Facing Systems

When a customer-facing customer support model generates biased or toxic completions, the company faces immediate reputational and legal risks. The Governance Panel must ensure that all customer-facing systems utilize real-time toxicity filters that analyze the model’s outputs before they are displayed to the user. If the filter detects toxic content or policy violations, the system blocks the completion, returns a standardized fallback response, and triggers a Level 1 incident. The incident response team must then audit the model’s prompts and parameters to identify the source of the failure.Managing Model Drift in Financial Underwriting Systems

In financial underwriting systems, minor model drift can result in substantial loan default losses or regulatory violations. The risk management team must continuously compare the distribution of credit scores generated by the production model against the training baseline. If the Population Stability Index (PSI) flags a statistical drift, the system must automatically route underwriting decisions to human loan officers for manual review. The model is then scheduled for retraining on the new dataset, and the performance outcomes are documented in the immutable WORM registry.Audit Trails for Human-in-the-Loop Override Actions

The Governance Panel requires a complete audit trail for all human-in-the-loop overrides. When an operator overrides a model’s decision (such as approving a transaction that the model flagged as fraudulent), the system must prompt the operator to select a predefined justification code and input detailed comments. The operator’s ID, the model’s original output, the override action, and the justification are signed with a cryptographic hash and written to the WORM database. This audit trail is reviewed by external auditors during ISO 42001 certification reviews.Post-Incident Remediation and Lessons Learned

Following any Level 1 or Level 2 incident, the engineering and risk teams must conduct a formal post-incident review. The review must document:- Root Cause Analysis: The underlying technical failure that caused the incident (e.g., training data contamination, unhandled edge cases in user prompts).

- Impact Assessment: The financial, legal, and reputational damage caused by the incident.

- Remediation Steps: The actions taken to resolve the immediate issue and prevent future occurrences.

- Governance Updates: Recommendations for modifying the risk classification registry or updating safety policies.

Incident Response C4.3: Mitigating Bias and Toxicity in Customer-Facing Systems

When a customer-facing customer support model generates biased or toxic completions, the company faces immediate reputational and legal risks. The Governance Panel must ensure that all customer-facing systems utilize real-time toxicity filters that analyze the model’s outputs before they are displayed to the user. If the filter detects toxic content or policy violations, the system blocks the completion, returns a standardized fallback response, and triggers a Level 1 incident. The incident response team must then audit the model’s prompts and parameters to identify the source of the failure.Managing Model Drift in Financial Underwriting Systems

In financial underwriting systems, minor model drift can result in substantial loan default losses or regulatory violations. The risk management team must continuously compare the distribution of credit scores generated by the production model against the training baseline. If the Population Stability Index (PSI) flags a statistical drift, the system must automatically route underwriting decisions to human loan officers for manual review. The model is then scheduled for retraining on the new dataset, and the performance outcomes are documented in the immutable WORM registry.Audit Trails for Human-in-the-Loop Override Actions

The Governance Panel requires a complete audit trail for all human-in-the-loop overrides. When an operator overrides a model’s decision (such as approving a transaction that the model flagged as fraudulent), the system must prompt the operator to select a predefined justification code and input detailed comments. The operator’s ID, the model’s original output, the override action, and the justification are signed with a cryptographic hash and written to the WORM database. This audit trail is reviewed by external auditors during ISO 42001 certification reviews.Post-Incident Remediation and Lessons Learned

Following any Level 1 or Level 2 incident, the engineering and risk teams must conduct a formal post-incident review. The review must document:- Root Cause Analysis: The underlying technical failure that caused the incident (e.g., training data contamination, unhandled edge cases in user prompts).

- Impact Assessment: The financial, legal, and reputational damage caused by the incident.

- Remediation Steps: The actions taken to resolve the immediate issue and prevent future occurrences.

- Governance Updates: Recommendations for modifying the risk classification registry or updating safety policies.

Incident Response C4.4: Mitigating Bias and Toxicity in Customer-Facing Systems

When a customer-facing customer support model generates biased or toxic completions, the company faces immediate reputational and legal risks. The Governance Panel must ensure that all customer-facing systems utilize real-time toxicity filters that analyze the model’s outputs before they are displayed to the user. If the filter detects toxic content or policy violations, the system blocks the completion, returns a standardized fallback response, and triggers a Level 1 incident. The incident response team must then audit the model’s prompts and parameters to identify the source of the failure.Managing Model Drift in Financial Underwriting Systems

In financial underwriting systems, minor model drift can result in substantial loan default losses or regulatory violations. The risk management team must continuously compare the distribution of credit scores generated by the production model against the training baseline. If the Population Stability Index (PSI) flags a statistical drift, the system must automatically route underwriting decisions to human loan officers for manual review. The model is then scheduled for retraining on the new dataset, and the performance outcomes are documented in the immutable WORM registry.Audit Trails for Human-in-the-Loop Override Actions

The Governance Panel requires a complete audit trail for all human-in-the-loop overrides. When an operator overrides a model’s decision (such as approving a transaction that the model flagged as fraudulent), the system must prompt the operator to select a predefined justification code and input detailed comments. The operator’s ID, the model’s original output, the override action, and the justification are signed with a cryptographic hash and written to the WORM database. This audit trail is reviewed by external auditors during ISO 42001 certification reviews.Post-Incident Remediation and Lessons Learned

Following any Level 1 or Level 2 incident, the engineering and risk teams must conduct a formal post-incident review. The review must document:- Root Cause Analysis: The underlying technical failure that caused the incident (e.g., training data contamination, unhandled edge cases in user prompts).

- Impact Assessment: The financial, legal, and reputational damage caused by the incident.

- Remediation Steps: The actions taken to resolve the immediate issue and prevent future occurrences.

- Governance Updates: Recommendations for modifying the risk classification registry or updating safety policies.

Incident Response C4.5: Mitigating Bias and Toxicity in Customer-Facing Systems

When a customer-facing customer support model generates biased or toxic completions, the company faces immediate reputational and legal risks. The Governance Panel must ensure that all customer-facing systems utilize real-time toxicity filters that analyze the model’s outputs before they are displayed to the user. If the filter detects toxic content or policy violations, the system blocks the completion, returns a standardized fallback response, and triggers a Level 1 incident. The incident response team must then audit the model’s prompts and parameters to identify the source of the failure.Managing Model Drift in Financial Underwriting Systems

In financial underwriting systems, minor model drift can result in substantial loan default losses or regulatory violations. The risk management team must continuously compare the distribution of credit scores generated by the production model against the training baseline. If the Population Stability Index (PSI) flags a statistical drift, the system must automatically route underwriting decisions to human loan officers for manual review. The model is then scheduled for retraining on the new dataset, and the performance outcomes are documented in the immutable WORM registry.Audit Trails for Human-in-the-Loop Override Actions