STRATEGIC OVERVIEW DeFi 2.0: The Rise of Sovereign Algorithmic Banking By Vatsal Shah · June 12, 2026 · Business / Finance Table of Contents 1. Introduction: Th…

Introduction: The Evolution of Sovereign Finance

Retail banking is facing a structural decline. Over the past decade, centralized commercial banks (CeFi) have struggled with legacy infrastructure, slow settlement timelines, and complex regulatory layers. The first wave of Decentralized Finance (DeFi 1.0) proved that lending, borrowing, and trading could operate without middlemen. However, it was plagued by high transaction fees, speculative yield farming bubbles, and smart contract vulnerability exploits.

The Limitations of DeFi 1.0

Under the first-generation DeFi framework, liquidity pools were notoriously capital-inefficient. Automated Market Makers (AMMs) spread capital uniformly across infinite price ranges ($0$ to $\infty$), meaning that only a small fraction of deposited capital was actively matched with trades at any given time. This resulted in high slippage, lower overall interest yields, and significant risk of Impermanent Loss for liquidity providers.Furthermore, traditional treasury systems were completely disconnected from these systems. Organizations faced complex compliance blocks when trying to route idle capital into on-chain protocols, meaning that cash reserves remained locked in centralized deposits yielding sub-inflationary rates.

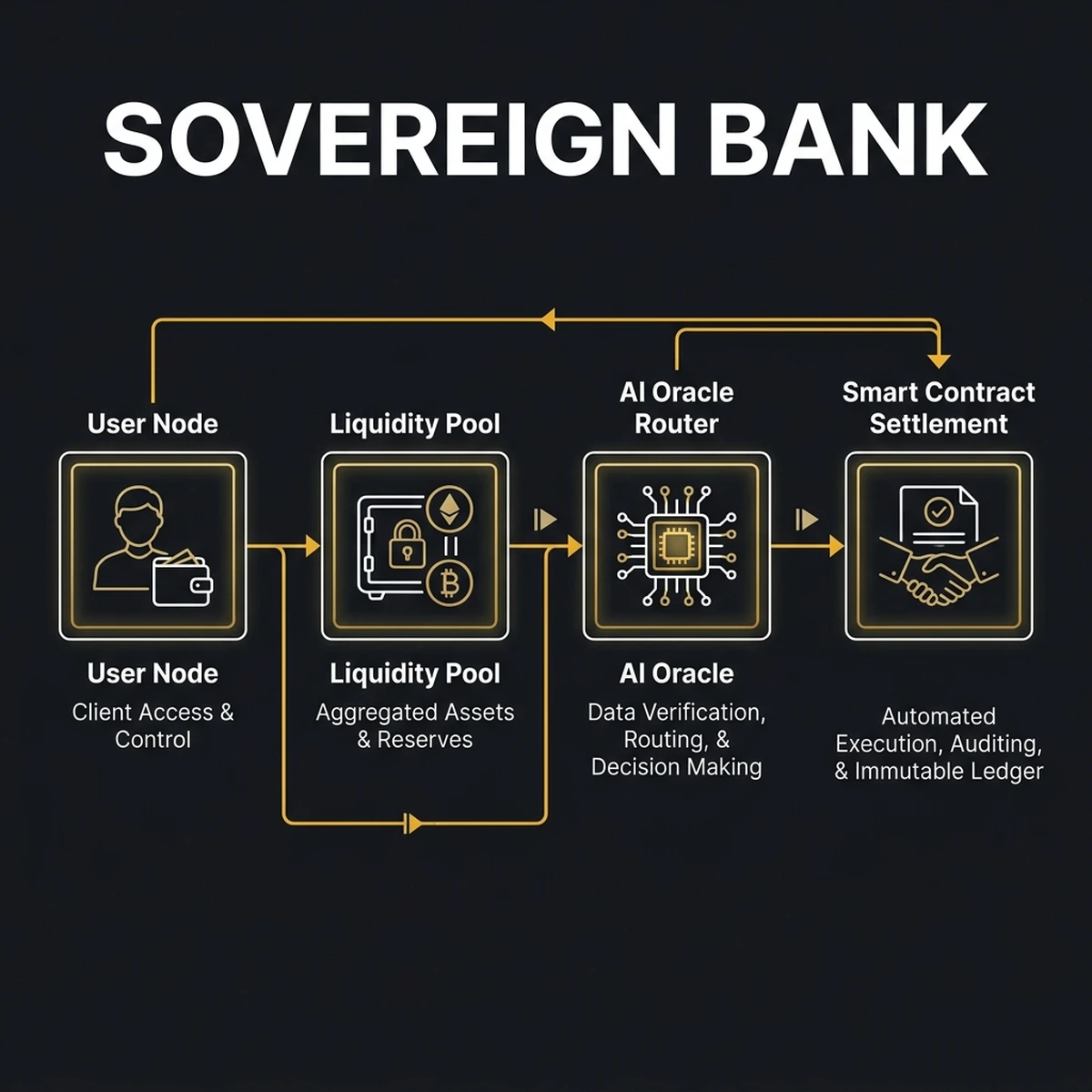

In 2026, the financial landscape is entering the era of DeFi 2.0. This phase is defined by Sovereign Algorithmic Banking. Rather than relying on human committees to adjust interest rates or verify loan applications, modern credit networks utilize decentralized liquidity pools controlled by real-time risk algorithms and smart contract engines.

For enterprise leaders, this shift offers a strategic advantage. Deploying cash reserves into sovereign lending protocols provides yield rates that outpace retail banks. Furthermore, smart contract platforms enable automated treasury management, letting companies route, hedge, and allocate capital across borders in milliseconds.

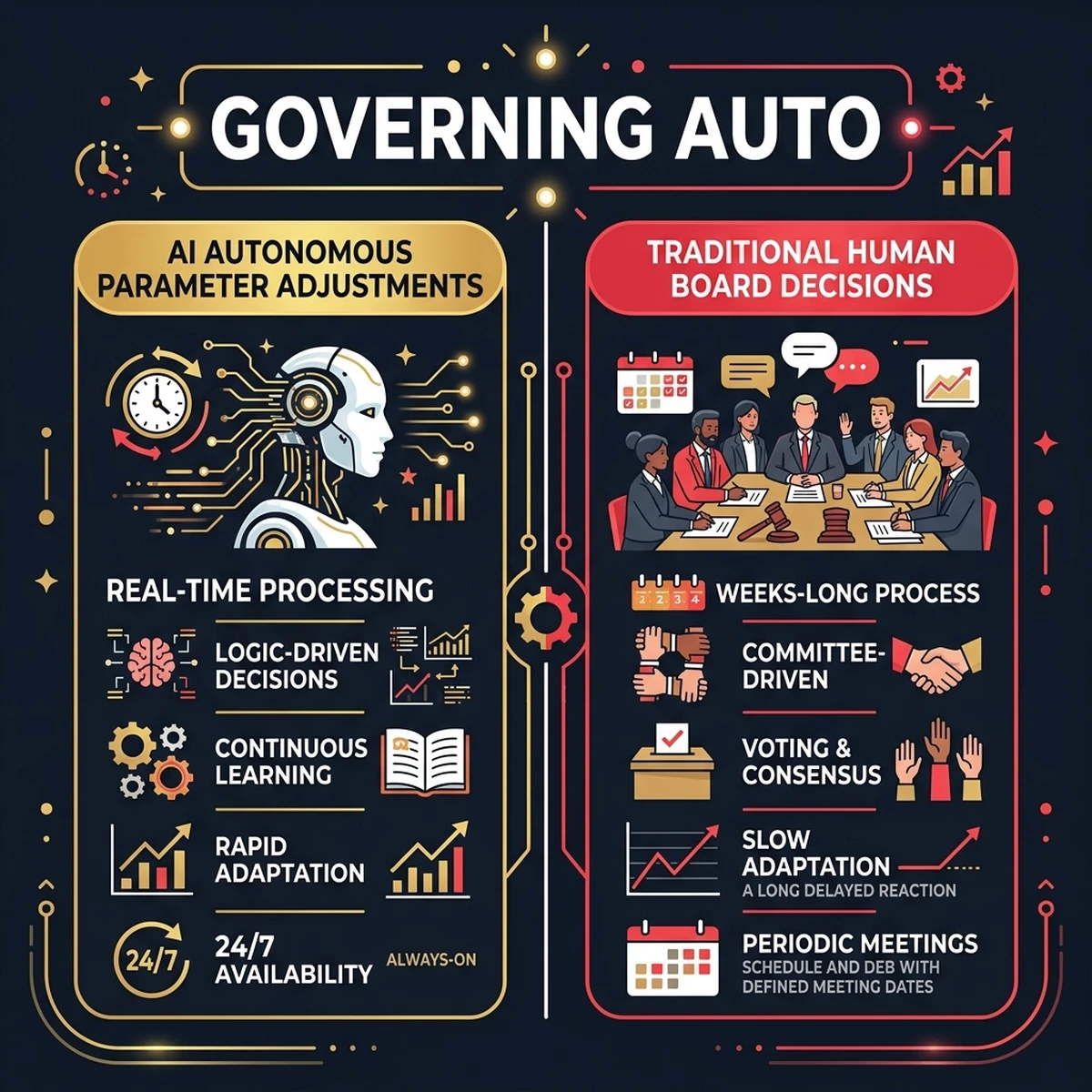

AI as the Board of Directors: Algorithmic Risk Management

In traditional banking, credit parameters—such as interest rate curves, loan-to-value (LTV) limits, and reserve ratios—are determined by credit committees during quarterly board meetings. This human-centric governance model is slow, reactive, and prone to error.

Programmatic Parameter Tuning

DeFi 2.0 protocols replace boards with autonomous risk systems. These algorithms continuously monitor pool liquidity, token volatility, and macroeconomic credit data.Interest rate adjustments are modeled dynamically using the Utilization Rate ($U$) of the liquidity pool:

$$U = \frac{\text{Borrows}}{\text{Total Available Liquidity}}$$

The interest rate ($R_t$) is adjusted programmatically depending on whether the utilization rate is below or above an optimal utilization threshold ($U_{\text{optimal}}$):

$$\text{If } U < U_{\text{optimal}}: \quad R_t = R_0 + \left( \frac{U}{U_{\text{optimal}}} \right) \times R_{\text{slope1}}$$

$$\text{If } U \geq U_{\text{optimal}}: \quad R_t = R_0 + R_{\text{slope1}} + \left( \frac{U - U_{\text{optimal}}}{1 - U_{\text{optimal}}} \right) \times R_{\text{slope2}}$$

Here, $R_0$ is the base rate, $R_{\text{slope1}}$ represents the gradual interest climb under normal borrowing limits, and $R_{\text{slope2}}$ is a steep interest spike applied when utilization crosses the optimal threshold. This steep increase protects the pool from running out of available withdrawal liquidity, automatically correcting capital balance without human intervention.

Guarding Against Liquidation Cascades

A key vulnerability of early DeFi was the liquidation loop. When asset prices fell rapidly, automated liquidations flooded the market, driving prices down further.Algorithmic banking protocols in 2026 utilize intelligent matching engines that absorb liquidations smoothly. These systems route liquidated assets into secondary markets gradually or lock them in insurance vaults, protecting pool depositors from systemic bad debt.

Furthermore, agents running simulation models (Agent-Based Modeling) run continuous stress tests on pool parameters. By executing millions of simulated market crashes per second, these systems predict slippage and adjust capital collateral ratios ahead of actual market movements, transforming risk mitigation from reactive to predictive.

Programmable Money for Agents: Cryptographic Wallets for Machine Labor

As businesses deploy autonomous agents to write code, manage supply chains, and execute marketing campaigns, a fundamental problem arises: How does an AI agent pay for its operations?

Traditional bank accounts require human signatures, physical IDs, and compliance reviews. An AI agent cannot open a standard Chase or HSBC account. To enable machine-to-machine commerce, agents need self-custodial blockchain wallets.

1. Key Management Services (KMS) & MPC

To prevent security breaches, agents do not hold their private keys directly. Instead, they use Multi-Party Computation (MPC) or secure local Key Management Services (KMS).MPC represents a major evolutionary leap over traditional multi-signature setups. In a multi-sig environment, multiple separate transactions must be compiled, signed, and broadcast to the blockchain, incurring high gas fees and exposing which individual keys participated in the signature. MPC solves this by executing a off-chain signature loop. The private key is split mathematically into key shares (using Shamir's Secret Sharing schemes). When the agent requests a transaction, the shares compute their local signatures, and a single, standard cryptographic signature is submitted to the blockchain, keeping the execution logic private and saving significant gas.

Additionally, Zero-Knowledge Proofs (ZKPs) can be integrated into the MPC workflow. This allows the agent to prove that its transaction complies with internal corporate budget guidelines without exposing the underlying call details, purchase amounts, or vendor addresses to the public ledger.

Below is an architectural configuration schema for an MPC transaction authorization loop:

{

"transaction": {

"to": "0x742d35Cc6634C0532925a3b844Bc454e4438f44e",

"value": "1250000000000000000",

"data": "0xa9059cbb000000000000000000000000...",

"maxFeePerGas": "35000000000",

"maxPriorityFeePerGas": "1500000000"

},

"kms_authorization": {

"agent_id": "agent_billing_node_09",

"session_token": "sess_89f0a2d3e911",

"policy_check": {

"budget_limit_usd": 150.00,

"daily_spend_current_usd": 42.50,

"rule_match": "allow_approved_saas_vendors"

},

"cryptographic_shares": {

"share_index": 2,

"required_signatures": 2,

"threshold": 2

}

}

}2. ERC-4337 Account Abstraction

Sovereign finance utilizes Account Abstraction (ERC-4337) to separate key control from account ownership. Rather than directly executing transactions from an externally owned account (EOA), agents interact via a smart contract wallet.The core interface centers around the UserOperation struct which specifies execution instructions (including gas parameters, paymaster signatures, and call data) sent to the central EntryPoint contract:

struct UserOperation {

address sender;

uint256 nonce;

bytes initCode;

bytes callData;

uint256 callGasLimit;

uint256 verificationGasLimit;

uint256 preVerificationGas;

uint256 maxFeePerGas;

uint256 maxPriorityFeePerGas;

bytes paymasterAndData;

bytes signature;

}This allows developers to write specific execution policies directly into the wallet contract:

- Daily Spending Limits: Restricts the maximum value an agent can transfer per 24 hours.

- Tool-Based Allowlists: Only allows transaction executions triggered by verified tools (e.g. git, npm, or custom build scripts).

- Automated Gas Sponsorship (Paymasters): Allows enterprise billing accounts to pay gas fees in stablecoins, shielding the agent from needing to hold native gas tokens like ETH.

SovereignPaymaster validates and sponsors an agent's transaction fee:

// SPDX-License-Identifier: MIT

pragma solidity ^0.8.20;

interface IPaymaster {

function validatePaymasterUserOp(

UserOperation calldata userOp,

bytes32 userOpHash,

uint256 maxCost

) external returns (bytes memory context, uint256 validationData);

}

contract SovereignPaymaster is IPaymaster {

address public owner;

mapping(address => bool) public approvedAgents;

constructor() {

owner = msg.sender;

}

function setAgentStatus(address agent, bool approved) external {

require(msg.sender == owner, "Only owner");

approvedAgents[agent] = approved;

}

function validatePaymasterUserOp(

UserOperation calldata userOp,

bytes32 userOpHash,

uint256 maxCost

) external view override returns (bytes memory context, uint256 validationData) {

// Validate if the agent sender is on our approved list

if (!approvedAgents[userOp.sender]) {

return ("", 1); // Signature/Validation fail code

}

// Return 0 indicating success, fee sponsored by the paymaster deposit

return ("", 0);

}

}The Unbanked Enterprise: Bypassing Centralized Retail Channels

Sovereign finance allows startups and global enterprises to operate completely outside the traditional banking system. By utilizing stablecoin networks (such as USDC or PYUSD) and decentralized money markets, companies can run treasury, payroll, and vendor billing on-chain.

Bypassing Cross-Border Friction

A global business paying remote developers in 15 countries normally struggles with high wire fees, unfavorable currency exchange rates, and days-long settlement delays.Using the sovereign stack, payroll is processed in seconds over high-throughput Layer 2 networks. Transactions cost less than $0.05, and funds are settled immediately, allowing developers to withdraw cash or deposit it into local yield protocols without delay.

On-chain payroll streaming tools (like Sablier or custom escrow contracts) allow businesses to stream compensation second-by-second. The funds are locked in the streaming escrow contract, and the developer can claim their accrued balance whenever they choose. This eliminates payment default risks and payroll processing overhead.

Sovereign Credit Lines and Invoice Factoring

Under the old model, securing an enterprise credit line required months of audited financials, personal guarantees, and high interest rates.DeFi 2.0 money markets introduce algorithmic credit delegation. An enterprise can lock stablecoin collateral into a smart contract and borrow working capital immediately at market rates, bypassing credit history checks. The smart contract acts as the absolute escrow, guaranteeing payment and eliminating settlement risk.

Furthermore, businesses can use decentralized invoice factoring. An enterprise uploads a cryptographically signed purchase order to an on-chain protocol. The protocol evaluates the creditworthiness of the issuer smart contract and instantly advances stablecoins to the supplier, bypassing traditional banking factor desks and reducing liquidity cycle times from 90 days to under 2 minutes.

Additionally, these unbanked entities increasingly adopt legal wrappers designed for decentralized structures, such as a Wyoming Decentralized Unincorporated Nonprofit Association (DUNA) or custom LLC templates, ensuring legal liability limits while operating natively on-chain.

To secure these systems from arbitrage and manipulation, algorithmic protocols integrate decentralized oracle networks (such as Chainlink or Pyth). These networks aggregate price data from multiple independent off-chain sources and submit them using cryptographic proofs. This protects lending pools from oracle manipulation attacks, flash loan arbitrage exploits, and sandwich attacks, ensuring that borrow and liquidation triggers are based on the absolute market median price.

Bypassing ERP and Treasury Silos

Traditional corporate treasury departments manage assets manually through spreadsheet entries and periodic bank portal audits. DeFi 2.0 banking protocols connect natively to enterprise ERP stacks (such as SAP or Microsoft Dynamics 365) via Model Context Protocol (MCP) gateways.An autonomous treasury agent can continuously scan accounts payable ledgers in the ERP, verify payment parameters against oracle data, swap stablecoins dynamically via liquidity pools, and trigger immediate cross-border settlements over Layer 2. The agent then registers the transaction hash and associated gas fees natively back to the ERP ledger, creating a closed-loop financial system with zero human data entry.

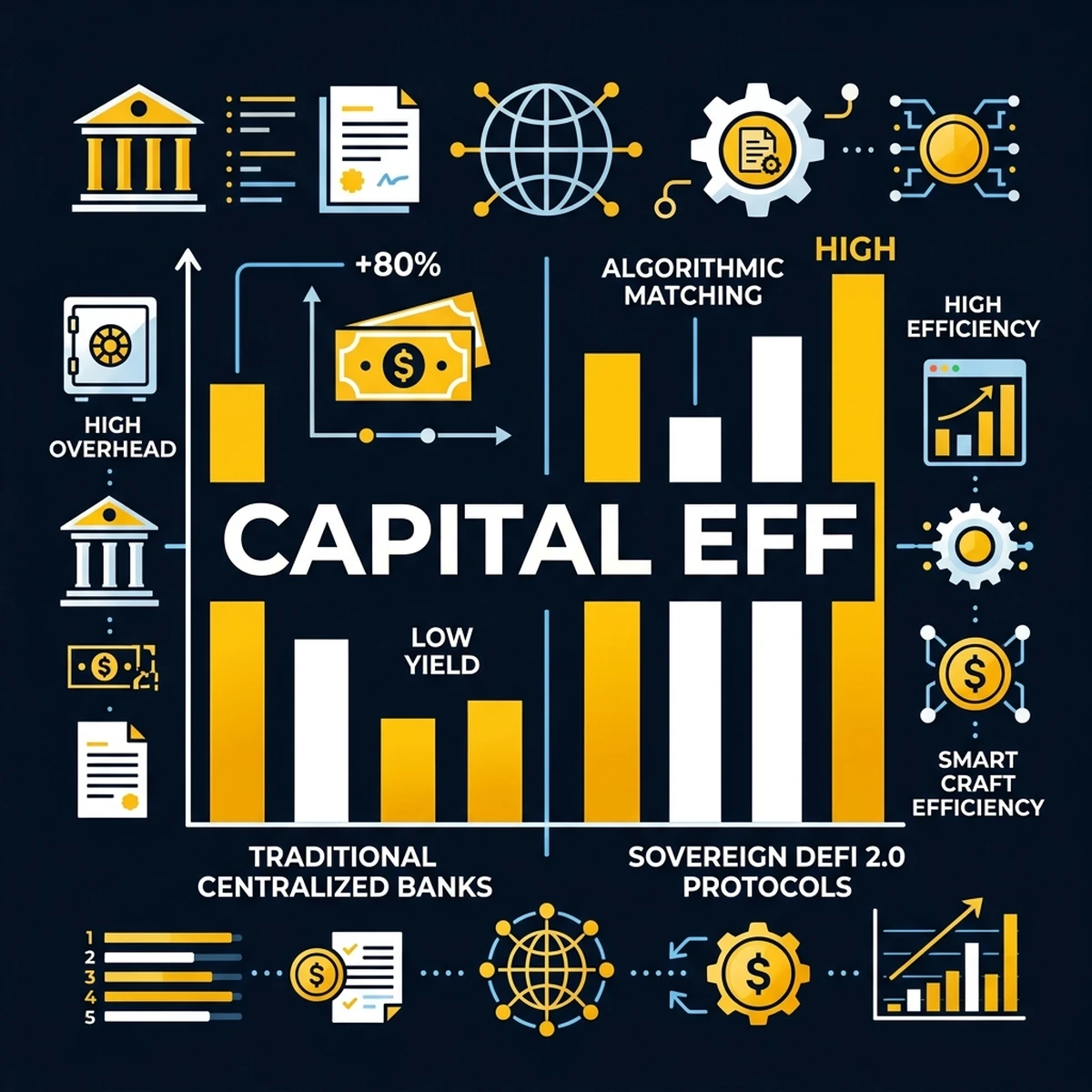

Comparative Analysis: Centralized Finance vs. Sovereign DeFi 2.0

To evaluate the operational transition to sovereign banking, we compare the structural profiles of Centralized Finance (CeFi) and DeFi 2.0 protocols.

Traditional retail channels operate under massive overhead burdens, including building lease fees, employee salaries, and manual compliance auditing costs. These costs are transferred to customers via high wire fees, low interest yields on savings accounts, and strict borrowing limits.

In contrast, DeFi 2.0 protocols are run by software code. Lending matches occur algorithmically without credit review desks. This efficiency allows protocols to return up to 95% of generated yield directly to depositors, leaving only a minor percentage to cover protocol reserves.

| Feature Category | Traditional Retail Banking (CeFi) | Sovereign Algorithmic Banking (DeFi 2.0) |

|---|---|---|

| Average Settlement Time | 1 to 5 business days | 1 to 15 seconds (on-chain) |

| Transaction Cost Profile | $15 - $45 per wire transfer | Under $0.05 (Layer 2 gas fees) |

| Risk Governance Mechanism | Manual quarterly credit board reviews | Real-time programmatic smart contracts |

| Agent / Machine Compatibility | Banned (Requires physical identity) | Native (KMS/MPC signed accounts) |

| Capital Yield Rate (Stablecoins) | 0.01% - 1.5% APY | 4.5% - 8.2% APY (algorithmic pools) |

Conclusion & Next Steps

The transition to DeFi 2.0 represents a fundamental shift in how enterprises manage, deploy, and interact with money. By replacing centralized intermediaries with secure smart contracts and AI-governed credit systems, organizations can build automated, capital-efficient, and secure financial operations.

Strategic Roadmap for Enterprises:

- Stablecoin Integration: Transition a portion of corporate reserves into high-security stablecoins (such as USDC) to bypass traditional cross-border settlement fees.

- Agentic Wallet Setup: Deploy local KMS/MPC infrastructure to enable your autonomous software agents to pay for compute and services independently.

- Lending Pool Auditing: Select audited, battle-tested money market protocols (like Aave V4) to generate capital yield on cash assets.

- Governance Hardening: Implement smart contract parameters and local multisig guardrails to prevent unauthorized treasury transfers.

Frequently Asked Questions

1. Is DeFi 2.0 safe from smart contract hacks?

While security has improved significantly with advanced multi-sig controls and automated auditing tools, smart contract risk remains. Before integrating any protocol, ensure it has passed multiple independent third-party audits and holds a solid historical track record of securing funds.2. Can traditional businesses integrate with sovereign finance?

Yes. Off-ramps and on-ramps allow companies to convert stablecoins back to fiat currency in seconds. This allows you to manage operations on-chain while settling taxes and regulatory payments in fiat.3. What is the impact of central bank digital currencies (CBDCs)?

CBDCs will likely accelerate on-chain enterprise adoption. By introducing government-backed digital fiat, corporations can settle deals and run treasury operations natively on-chain without exchange rate volatility.4. How do MPC wallets protect AI agents from losing funds?

MPC wallets split the private key into multiple distinct shares. The agent only holds one share, while the server/KMS holds the others. The agent cannot sign a transaction without the server's approval, preventing unauthorized transfers if the agent is compromised.5. What are the tax implications of running an on-chain business?

Transactions on the blockchain are public and immutable. By utilizing automated accounting tools, every transaction can be categorized, parsed, and logged for tax filings, making audits simpler than traditional manual reporting.6. How does algorithmic lending prevent default risk?

All loans in DeFi 2.0 protocols are backed by excess collateral. If a borrower's collateral value falls below the minimum ratio, the smart contract automatically sells the collateral to repay the loan, ensuring the pool is always solvent.About the Author

Vatsal Shah is a software architect, AI developer, and technology consultant specializing in decentralized infrastructure, sovereign cloud architectures, and machine learning deployments. He builds and designs local-first tech systems for enterprise customers globally.